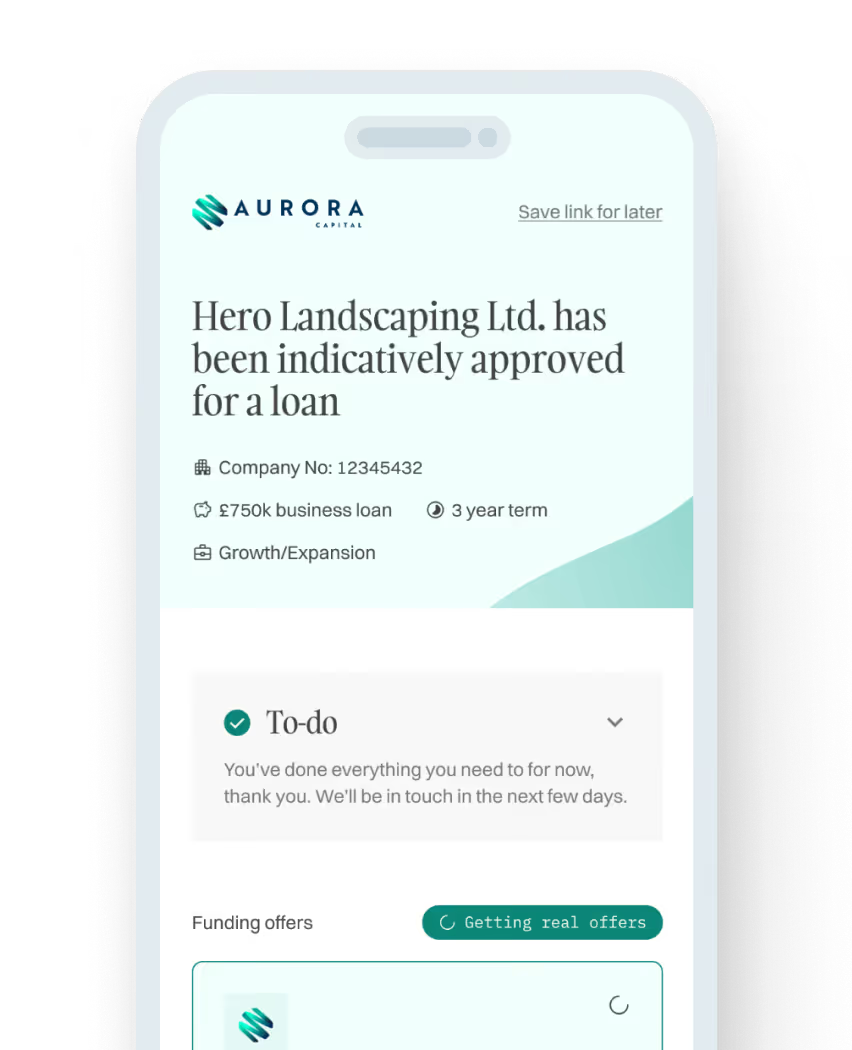

Our LendTech platform lets you:

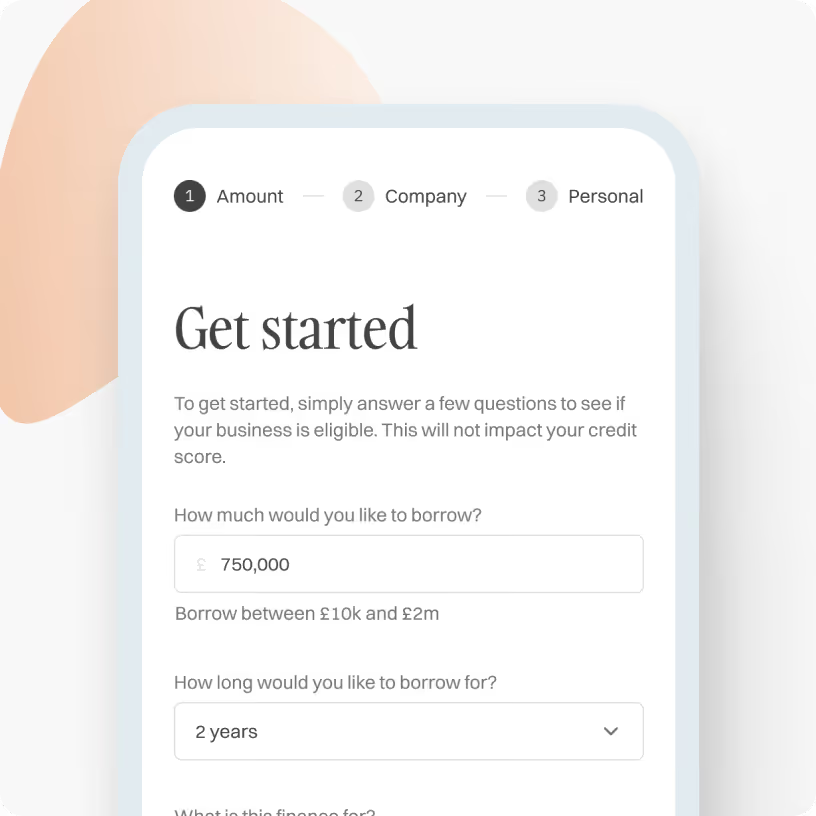

Check eligibility in 30 seconds

Match with 50+ lenders

Get indicative offers in 5 mins

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Asset Finance Loans

If you need to purchase new equipment or assets but don’t want to impact your cash flow or don’t have the immediate capital available, an asset finance agreement could be the solution you’re looking for. Learn more about how asset finance could help you invest in your business and compare rates from top asset finance lenders with Aurora Capital.

.svg)

What is asset finance?

Asset finance allows businesses to acquire the assets they need to operate and grow, such as machinery, vehicles, and equipment.

Using asset finance means your business can get important assets without needing to raise a lump sum to purchase them. You can spread the cost of a new asset over time, making it easier to manage without impacting your cash flow.

Key features of asset finance

- Suitability: Any business that needs to purchase any asset without the need for upfront capital or wanting to raise funds by refinancing an existing asset.

- Purpose: Used to either lease or purchase an asset.

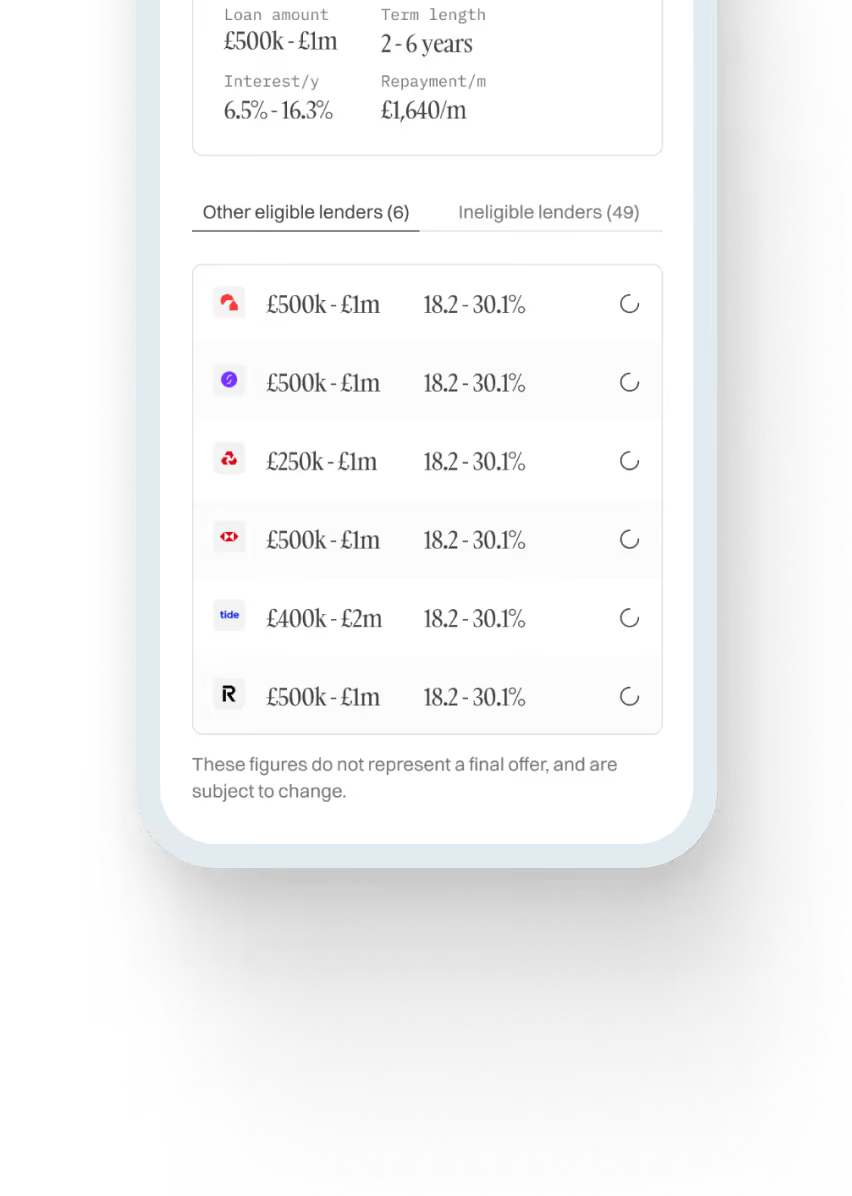

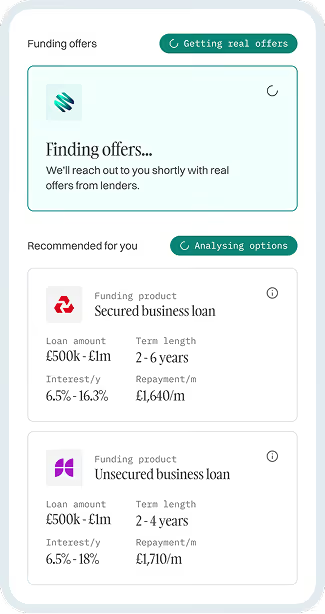

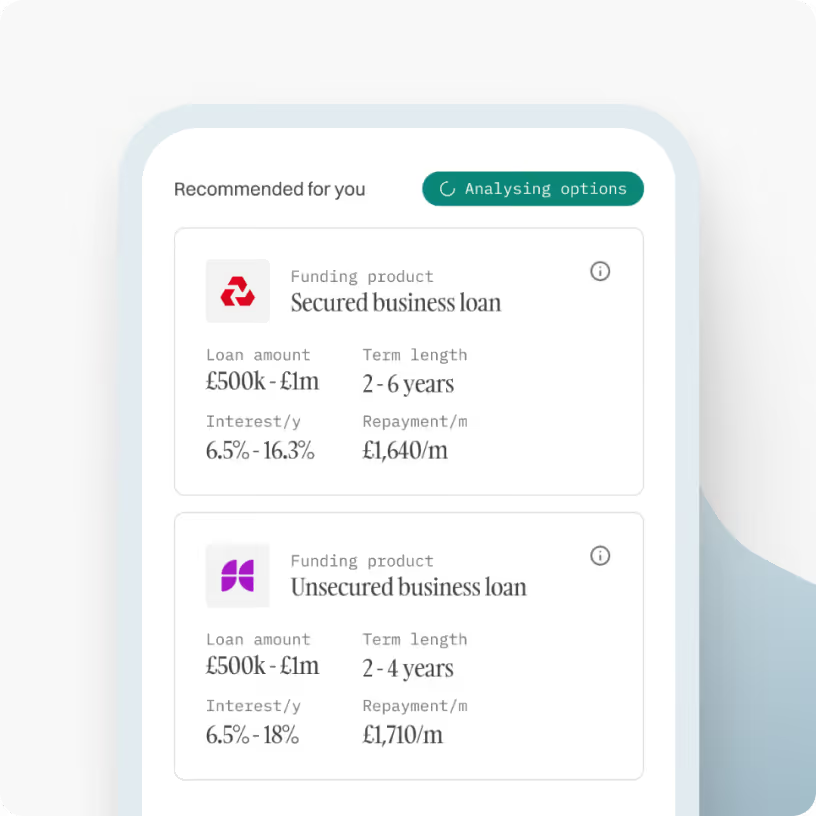

- Amount: Loans can range from £1k – £2m, depending on the type of asset and affordability.

- Term: Up to 7 years, depending on the type of asset and creditworthiness of the business.

- Cost: Variable, interest rates start from 6%.

- Security: The asset is secured until a full repayment has been made. Some lenders may also ask for a personal guarantee.

- Speed: Applications can be processed within 24 hours of receiving a full proposal.

What assets can you finance?

A business can finance two types of assets: hard and soft assets. Whether an asset is considered hard or soft depends on its resale value.

Hard assets are usually high value and hold their value if they are used, whereas soft assets typically have little value by the end of the finance term.

- Hard assets: These are typically machines such as agricultural machinery, vehicles, or manufacturing equipment.

- Soft assets: These assets can be catering equipment, gymnasium equipment, medical equipment, or IT software.

While it is possible to finance both types of assets, most lenders will have a preference over what they can finance.

Get a free, no obligation quote

Apply in minutes, there’s no impact on your credit score and you’ll get a free, no obligation personalised quote in hours. Regulated by the FCA: 831395

How much would you like to borrow?

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Prefer to talk? Call us on 01371870815

.svg)

Frequently asked questions

Is asset-based lending right for your business?

Asset-based lending can be a good fit if your business has assets that can help you access the finance you need.

It is often used by businesses that sell to other companies, hold valuable stock, or need working capital that can change as activity increases.

You will need assets that are easy to value and for which you can maintain strong records, because lenders usually require ongoing reporting to keep the facility.

It may be less suitable if you want a simple one-off loan, or if your business has limited eligible assets. In those cases, a fixed-term unsecured loan or another type of business finance may be a better fit.

Types of asset finance

The asset finance product you choose for your business will depend on whether you want to own, rent or release cash tied up in assets you already own. Here’s a breakdown of the different asset finance and equipment loan options you can choose from:

Hire purchase

Hire purchase (HP) is a way to buy a new or used asset without paying for it upfront. You effectively hire the asset from the lender and pay it off in instalments so that you own it outright by the end of the agreement. HP can be used to buy most business assets and is a popular form of business van finance.

The asset usually appears as a positive item on your balance sheet from the start of the agreement, but the provider owns the asset until the last instalment is paid.

This means you cannot sell the asset during the term. However, you may need to pay a purchase option fee at the end of the term to transfer ownership of the asset to you; this fee can be as low as £1. It’s important to remember that you will be responsible for the asset’s upkeep for the length of the agreement.

Finance lease

A finance lease, also known as an equipment lease, is an agreement in which a leasing firm buys a business asset on your behalf and then rents it to your business.

You make regular scheduled payments for the use of the asset. At the end of the agreed term, you can extend the lease, return the asset to the lender, upgrade the item, or buy it outright by making a balloon payment.

Finance leasing can be used for most business assets, from laptops and printers to commercial vehicles and machinery. Equipment lease agreements are based on the asset's depreciation, not the full cost price, so the monthly payments are typically lower than hire purchase.

However, if you decide to purchase the equipment by making a balloon payment at the end of the agreement, it will be more expensive than if you had purchased it outright.

Equipment leasing can offer potential tax advantages as you can offset 100% of your monthly payments against your corporation tax bill.

Asset refinance

Asset refinancing, also known as a sale and leaseback agreement, is a way of accessing money tied to your business's existing assets. It differs from asset finance in that you borrow against your existing assets to access funding rather than acquiring a new asset.

You effectively sell an asset to the lender for an agreed sum based on its current value and then lease it back from them. You make monthly payments for the term of the agreement, and at the end of the term, you will usually retake ownership of the asset.

One advantage of asset refinance is that you don’t need to own the asset you use as security. For example, if you purchased machinery through an HP agreement worth £10,000 and still owe £2,000, the asset refinance company can settle the balance to take ownership of the asset. They can lend you a percentage of the asset’s value, usually around 70%.

Asset refinance is similar to a secured business loan. If you cannot make the monthly payments, the asset refinancing company can take the asset back to recover the money you owe.

Contract hire

Contract hire is used for work vehicles and can be a cost-effective way of leasing new business vans and cars. The contract hire provider will source and maintain the vehicles on your behalf, saving your business time and effort.

You will make fixed rental payments over an agreed-upon term and return the vehicles at the end of the agreement. Leasing in this way can be cost-effective, as you pay for the vehicle’s depreciation during the lease period rather than its total value.

Contract hire can also have tax benefits, as you can claim up to 100% VAT back and offset up to 100% against corporation tax. How much you can claim back will depend on how the vehicle will be used and how eco-friendly it is.

Is my business eligible for asset finance?

Asset financing should be available to your business, provided you can prove you can meet your financial commitments. Most lenders will also stipulate that your business:

- Is UK-based and registered

- Has been operating for at least two years

- Has a turnover of over £10,000 a year

As with most types of business finance, the better your credit history is, the better your chances of acceptance are, especially if you want to go down the hire purchase route. Lenders will generally be looking to see if you can afford the repayments laid out in your terms and what the risk of lending to you is.

If you’re unsure which option best suits your needs, don’t hesitate to contact our team.

Pros and cons of asset finance

Asset finance can be a cost-effective way for your business to acquire new assets or release money, but it might not be suitable for everyone. To determine if asset finance is the right option for your business, consider the pros and cons.

Pros of asset finance

- Maintain cash flow: The upfront costs of most asset finance products are very small or even zero, which helps preserve your business’s cash flow and can free up capital.

- Easy budgeting: Payments for most asset finance products are fixed and paid monthly over a set period, making it easier for your business to budget.

- Quick access to assets: Asset financing can allow your business to quickly get the assets it needs rather than waiting to accumulate the funds needed to buy the asset outright.

- Low maintenance: The asset finance provider often covers the maintenance cost, so you don’t need to worry about extra maintenance costs.

Cons of asset finance

- Usage limits: As the asset finance provider owns the asset, they may set limits on its usage. For example, many lease vehicles have an annual mileage limit you need to keep to and covering over the limit could result in penalties.

- Asset at risk: If you cannot keep up with the payments, the provider can repossess the asset. This could leave your business without an asset it needs to operate.

- Limited flexibility: Depending on your agreement, you may be unable to sell or upgrade the asset until the end of the term.

- Depreciation: The asset could depreciate in value faster than you can repay the loan, leaving you out of pocket.

How long can my business finance an asset for?

Asset finance is usually provided for anywhere between 1 and 7 years. The asset finance company recoups the purchase cost of the asset over the agreed period, plus interest.

The length of the finance agreement can also depend on how long the asset will be ‘usable’ for and how quickly the lender wants the money back. As a business borrower, you’ll have to show that your business can afford to make the agreed payments.

Is asset finance the same as asset refinancing?

Asset finance differs from asset refinancing in that it is used to acquire new machinery, equipment or vehicles, and asset refinancing is a way of borrowing against an asset that your business already owns.

How much can my business borrow through asset finance?

The amount you can borrow will depend on the asset you’re financing, your business’s credit record and the lender.

However, as a general rule, we finance equipment valued from £1k to £2 million. Lenders lend a percentage of the asset’s value, usually around 70%, but some can offer more.

What happens if I default on an asset finance agreement?

If you cannot keep up with your payments, the lender can take possession of the asset and use it to recover the amount you owe. In this way, asset finance is the same as any secured loan. However, the lender retains ownership of the asset for the duration of the agreement.

Defaulting on the loan will also have a negative impact on your credit score, making it harder to borrow in the future. If you are struggling to make your repayments, contact the lender as soon as possible to discuss your options.

Can I refinance equipment or machinery that my business already owns?

Yes, you can. However, certain criteria surround the age and condition of the equipment that we will refinance. These can include the type of equipment and the date that you purchased it.

What type of businesses do you lend to?

We lend to all types of businesses. Whether you’ve been established for decades or months, we can provide asset finance for businesses of all sizes in all sectors.

Industrial sector businesses, such as those in plants, packaging, printing, processing, agriculture, construction, and technology, can all use asset financing and are among the most common types of businesses to apply.

How do I find a business asset funding lender?

We can help you find a business loan suited directly to your needs. We have relationships with multiple lenders who can provide fast and flexible business funding. We can offer a wide array of business loan types with numerous benefits and competitive rates.

Finding the right funding is often a long-winded process, with plenty of variables to consider from all the different providers. Our finance experts can help by providing you with the best deals and rates.

Finding the right funding is often a long-winded process, with plenty of variables to consider from all the different providers. Our finance experts can help, providing you with a list of the best deals and rates.

Don’t see your question? Send us a message or call us on 01371870815 to speak to one of our funding specialists quickly.

How the process works

[1]

Enquire and check eligibility

Enquire in under 30 seconds to find out if your business is eligible for funding. We only need basic information about your business.

Check eligibility now

[2]

Get matched to lenders

Our LendTech technology will compare over 50 lenders and match you with the most suitable finance options.

Check eligibility now

[3]

Obtain funding in 48 hours

Once you have fully submitted your proposal, one of our funding specialists will discuss the available options and help get you funded.

Check eligibility now

No items found.

No items found.

No items found.

Get a quote, fast

Lending period

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Growth Guarantee Scheme

An unsecured business loan backed by the government. Ideal for businesses looking to grow and expand.

- Amount£25,001 to £750,000

- TermsUp to 6 year terms

- InterestFrom 10% per annum

Start growing

Unsecured Business Loans

A flexible, unsecured business loan with no security on assets or property. Ideal for growth, cashflow or working capital needs.

- Amount£10,000 to £750,000

- TermsUp to 6 year terms

- InterestFrom 6.9% per annum

Get unsecured loan

Asset Finance

Whether you are looking to purchase machinery, equipment or vehicles, this could be the ideal solution for your business.

- Amount£5,000 to £750,000

- TermsUp to 6 years

- InterestFrom 6% per annum

Finance assets

Revolving Credit Facilities

Looking to have a facility where you can drawdown funds when and if you require them, this could be the perfect facility for you.

- Amount£1,000 to £1,000,000

- TermsUp to 3 years

- InterestFrom 1.5% per month

Access credit line

VAT/Tax Loans

Have an upcoming Vat or Tax bill? This could be the perfect facility to keep cashflow healthy and never have to make a big chunky HMRC payment again.

- Amount£10,000 to £750,000

- TermsUp to 1 year term

- InterestFrom 1% per month

Get VAT loan

Merchant Cash Advances

A perfect solution for businesses that take over £10k per month in card/online sales. Rather than paying a fixed monthly payment, repayments are taken as a % of future card sales.

- Amount£10,000 to £750,000

- TermsVariable

- InterestNo APR

Get cash advance

Secured Business Loans

Are you a new start-up business or are you looking to invest a larger sum into your business? By using a property as security, we can lend larger amounts over longer terms.

- Amount£25,000 to £2,000,000

- TermsUp to 15 years

- InterestFrom 10% per annum

Get secured loan

Small Business Loans

Compare small business loans to assist with purchasing stock, upgrading equipment, or just general working capital requirements.

- Amount£10,000 to £750,000

- TermsUp to 6 years

- InterestFrom 6.9% per annum

Get small business loan

.svg)

Guides to help you make the best financial decisions

Compare business funding options today, quickly and easily

Browse our range of business funding options to find out more and discover the one that best suits your business.

Compare funding options

Prefer to chat? Call us on 01371870815 to speak to our experts.

.svg)