No items found.

All business needs options

Van Finance

Get your business on the road with flexible van finance solutions. Find affordable finance tailored to your business vehicle needs.

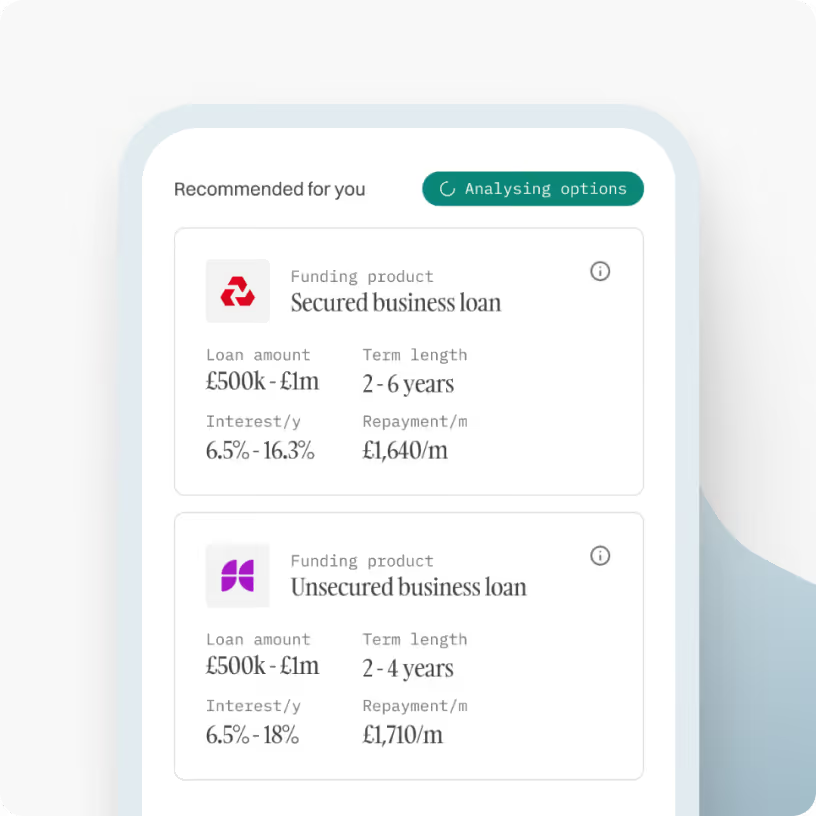

Our LendTech platform lets you:

Check eligibility in 30 seconds

Match with 50+ lenders

Get indicative offers in 5 mins

Check eligibility

Applying won't affect your credit score

Apply in minutes

Free, no-obligation quote

No effect on credit score

Get a quote, fast

Lending period

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Van finance

Using van finance can help your business get the work vehicle it needs to grow and thrive. Learn everything you need to know about how it works and see your funding options from top van finance providers with Aurora Capital.

What is van finance?

Van finance is a way of borrowing money from banks and financial institutions if your small business needs a van but can’t afford one immediately.

The work van that you use day-to-day is considered a business asset. Van finance can allow you to spread the cost of your work vehicle over time.

There are several different types of van finance available, and it can be difficult to determine which is best for your business. We break down everything you need to know about van finance so you can make the right decision.

Bridging loans are a type of secured loan, which means you will need to put up an asset as collateral.

Types of business van finance

There are a number of different van finance options available, including:

Business loan

It’s possible to use a standard unsecured business loan to purchase your van. Your business will need to borrow enough to cover the cost of the van upfront and then repay the loan over the agreed-upon term.

This option means there will be no usage restrictions, such as driving a certain number of miles each year. However, using a loan to buy your van can be more expensive and less flexible than other options.

Hire purchase

With hire purchase (HP), you put down a small deposit and then spread the remaining cost of the van over an agreed term. The deposit can be paid by cash, or you may be able to part exchange an old vehicle, provided you own it outright.

Your monthly payments will be based on the value of the vehicle, the interest rate charged, and the size of the deposit you put down.

You will own the vehicle outright at the end of the agreed term. HP agreements don’t usually come with any mileage limits, but there may be additional fees to pay at the end of the term.

Finance lease

Finance lease agreements are a flexible way of leasing a work vehicle. Your business can hire the vehicle for a specific period of time, and at the end of the agreement, you will have the option to:

- Purchase the van for a pre-agreed sum (known as a balloon payment)

- Sell the vehicle on the lender’s behalf and get a percentage of the proceeds

- Extend the term of the lease and continue the agreement

You can reclaim up to 100% of the VAT charged on your monthly payments, including mileage, maintenance, and any service costs.

.svg)

Get a free, no obligation quote

Apply in minutes, there’s no impact on your credit score and you’ll get a free, no obligation personalised quote in hours. Regulated by the FCA: 831395

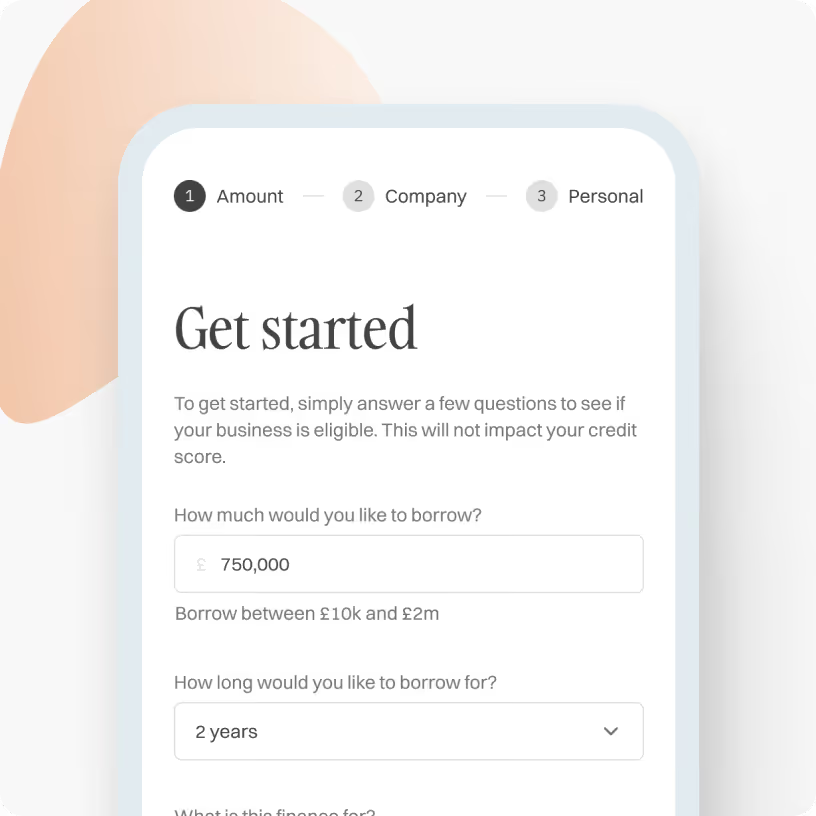

How much would you like to borrow?

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Prefer to talk? Call us on 01371870815

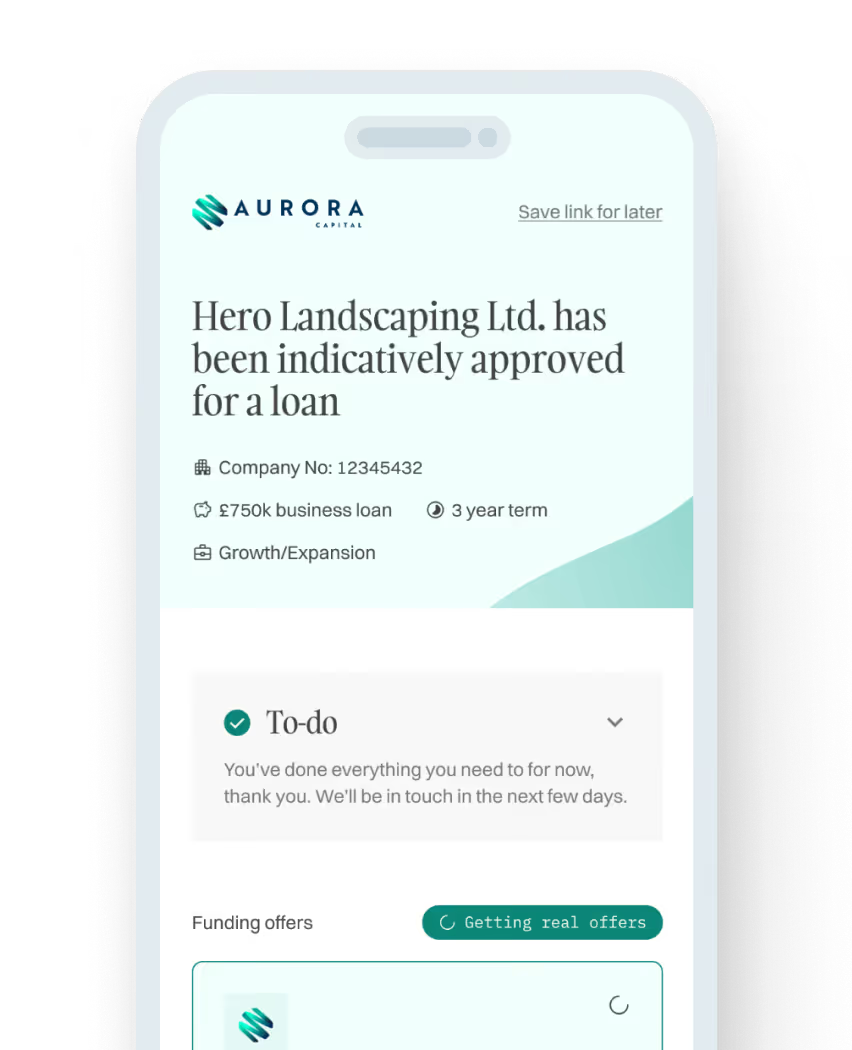

How the process works

[1]

Enquire and check eligibility

Enquire in under 30 seconds to find out if your business is eligible for funding. We only need basic information about your business.

Check eligibility now

[2]

Get matched to lenders

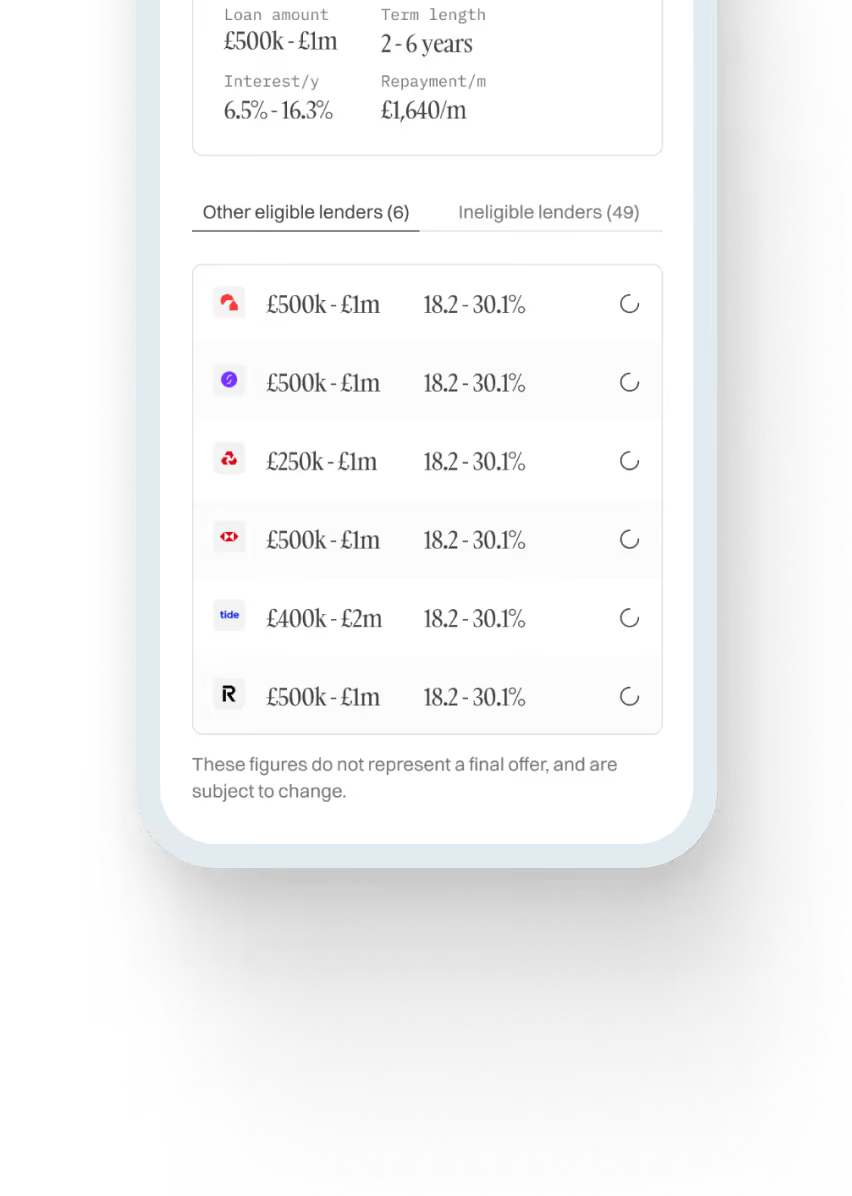

Our LendTech technology will compare over 50 lenders and match you with the most suitable finance options.

Check eligibility now

[3]

Obtain funding in 48 hours

Once you have fully submitted your proposal, one of our funding specialists will discuss the available options and help get you funded.

Check eligibility now

No items found.

No items found.

No items found.

How much could you borrow?

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Apply in minutes

Free, no-obligation quote

No effect on credit score

Growth Guarantee Scheme

An unsecured business loan backed by the government. Ideal for businesses looking to grow and expand.

- Amount£25,001 to £750,000

- TermsUp to 6 year terms

- InterestFrom 10% per annum

Start growing

Unsecured Business Loans

A flexible, unsecured business loan with no security on assets or property. Ideal for growth, cashflow or working capital needs.

- Amount£10,000 to £750,000

- TermsUp to 6 year terms

- InterestFrom 6.9% per annum

Get unsecured loan

Asset Finance

Whether you are looking to purchase machinery, equipment or vehicles, this could be the ideal solution for your business.

- Amount£5,000 to £750,000

- TermsUp to 6 years

- InterestFrom 6% per annum

Finance assets

Revolving Credit Facilities

Looking to have a facility where you can drawdown funds when and if you require them, this could be the perfect facility for you.

- Amount£1,000 to £1,000,000

- TermsUp to 3 years

- InterestFrom 1.5% per month

Access credit line

VAT/Tax Loans

Have an upcoming Vat or Tax bill? This could be the perfect facility to keep cashflow healthy and never have to make a big chunky HMRC payment again.

- Amount£10,000 to £750,000

- TermsUp to 1 year term

- InterestFrom 1% per month

Get VAT loan

Merchant Cash Advances

A perfect solution for businesses that take over £10k per month in card/online sales. Rather than paying a fixed monthly payment, repayments are taken as a % of future card sales.

- Amount£10,000 to £750,000

- TermsVariable

- InterestNo APR

Get cash advance

Secured Business Loans

Are you a new start-up business or are you looking to invest a larger sum into your business? By using a property as security, we can lend larger amounts over longer terms.

- Amount£25,000 to £2,000,000

- TermsUp to 15 years

- InterestFrom 10% per annum

Get secured loan

Small Business Loans

Compare small business loans to assist with purchasing stock, upgrading equipment, or just general working capital requirements.

- Amount£10,000 to £750,000

- TermsUp to 6 years

- InterestFrom 6.9% per annum

Get small business loan

.svg)

Guides to help you make the best financial decisions

Compare business funding options today, quickly and easily

Browse our range of business funding options to find out more and discover the one that best suits your business.

Compare funding options

Prefer to chat? Call us on 01371870815 to speak to our experts.

.svg)