No items found.

All industry funding options

Keep your pub or restaurant thriving with flexible business finance solutions for refurbishments, equipment, staffing, stock, and cash flow support.

Our LendTech Platform lets you:

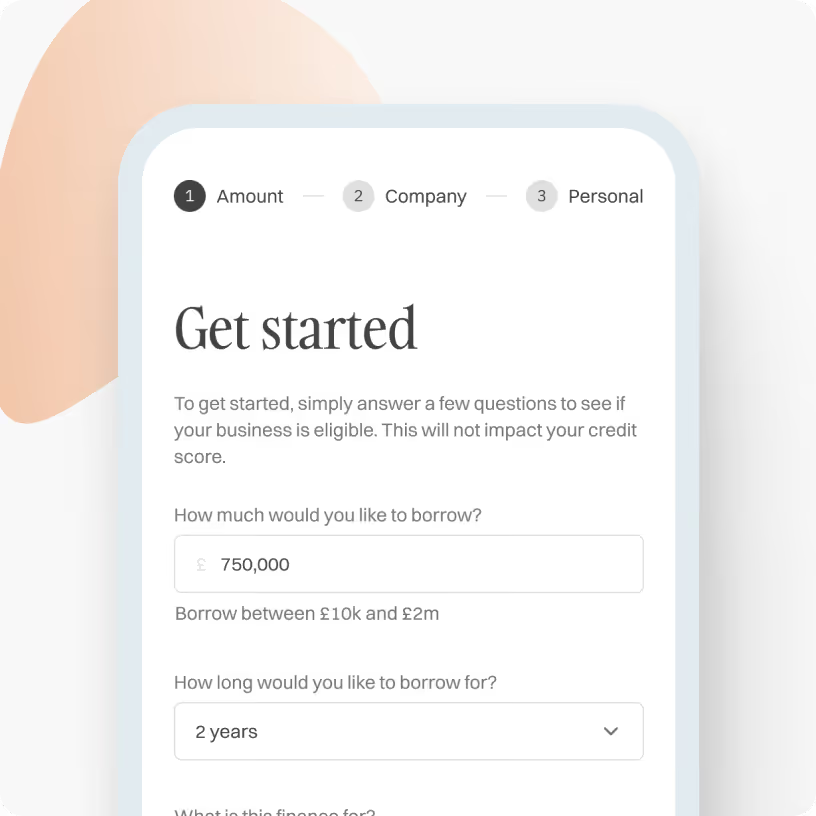

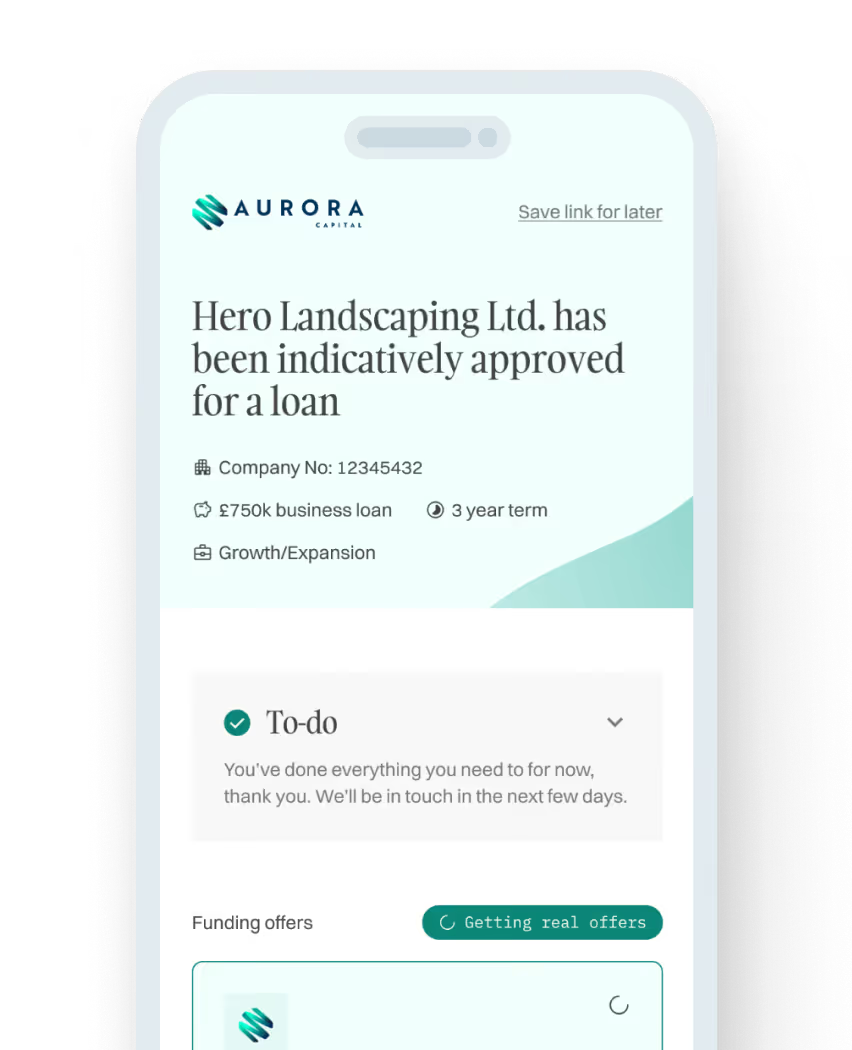

Check Eligibility in 30 seconds

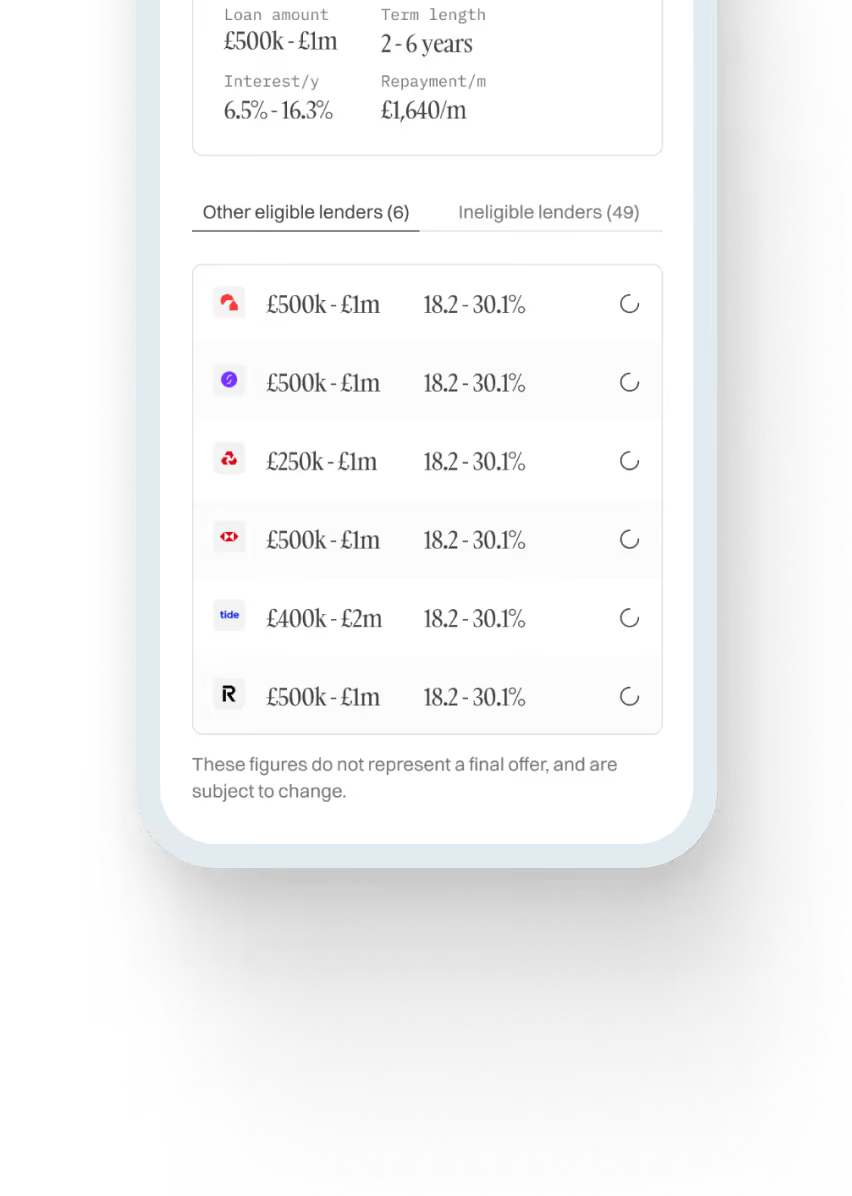

Match with 50+ lenders

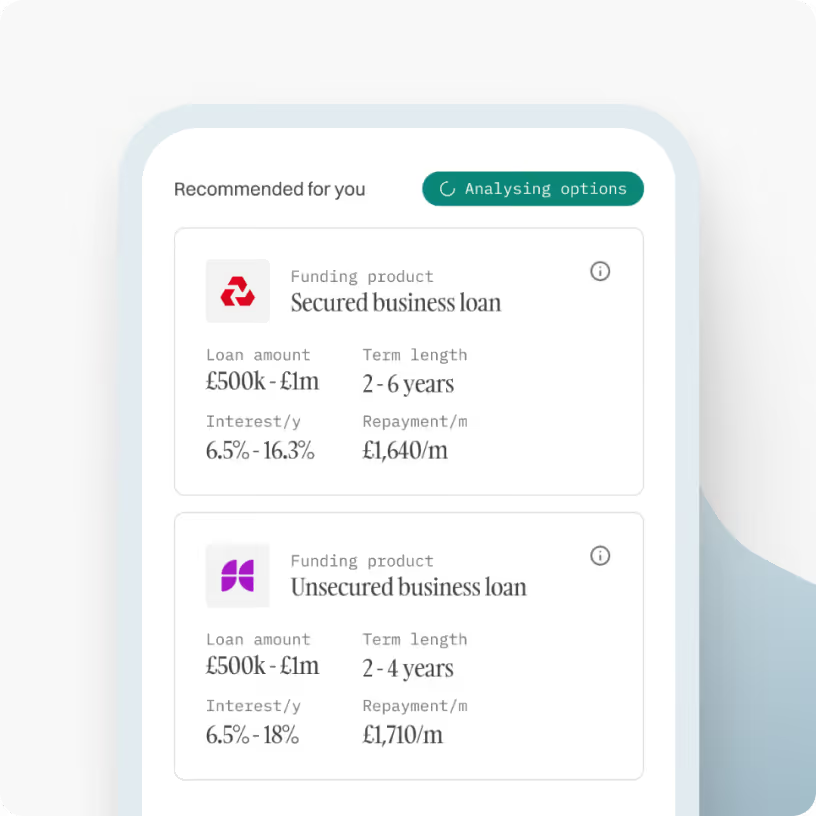

Get indicative offers in 5 mins

Apply in minutes

Free, no-obligation quote

No effect on credit score

What Finance Options Does Your Pub or Restaurant Have?

For pub and restaurant businesses, obtaining external funding can be vital to support growth and expansion, but not all credit lines are created equal, and it’s crucial to find the right solution that meets your specific needs.

At Aurora Capital, we specialise in identifying the most suitable funding solutions for this sector. We acknowledge that your funding needs may differ, so we offer a wide range of business loan options with varying eligibility requirements, funding amounts, and usage flexibility.

Whether you need to address a temporary cash flow challenge or secure financing to purchase new equipment or inventory, we have a funding solution that can meet your needs.

Asset Finance

Inevitably, sometimes your restaurant business will need to purchase new things, such as kitchen equipment, furniture, and so on. While these things can be expensive, it isn’t necessary to disrupt cash flow; asset finance allows you to acquire those assets, even if you don’t have the necessary funds readily available. Effectively, asset finance means you use business assets as collateral to secure funds and fuel growth, and it is seen by many as the best way to purchase restaurant-related equipment.

Find out more about asset finance

Unsecured Business Loans

Unsecured business loans can be an excellent alternative as they don’t require collateral, but it’s important to note that unsecured loans often have higher interest rates than secured loans, because lenders assume more risk due to the absence of collateral. Although you may not be able to borrow as much with an unsecured loan as you would with a secured loan, you can still obtain a significant amount of credit. Unsecured loans are versatile and can be used for any business-related expenses, making them an appropriate funding option for restaurants. These loans typically range from £1,000 to £500,000 and can be repaid over a maximum of six years.

Find out more about unsecured business loans

Recovery Loan Scheme

Recovery loans can offer essential assistance in overcoming financial difficulties. This form of borrowing is suitable for businesses that have encountered setbacks and need a significant amount of money to get back on track. Recovery loans usually range from £25,000 to £2 million and can be borrowed for a maximum period of six years.

Find out more about recovery loans

Merchant Cash Advance

Merchant cash advances can be an excellent solution for restaurants and pubs that experience fluctuations in revenue. Repayment of the advance and associated fees is typically made through automatic daily or weekly deductions from your credit card sales until the loan is entirely paid off. For instance, the lender may agree to deduct 10% of every card transaction until the loan and interest charges are fully repaid. As sales increase, the amount repaid grows, resulting in quicker loan repayment.

Find out more about merchant cash advances

Securing Pub and Restaurant Financing: The Importance of Business Loans

As a pub/restaurant owner, having access to business loans can be crucial for the success and growth of your establishment. Here are some reasons why:

- Staffing and Expenses: During quiet periods, it can be challenging to cover overhead expenses, such as rent, utilities and staff salaries. A business loan can provide the necessary funds to pay these costs and keep your restaurant running smoothly.

- Renovations and Expansion: As your pub/restaurant grows, you may want to renovate or expand your establishment. A business loan can help finance these projects, allowing you to create a more inviting and modern environment for your customers.

- Purchasing Inventory: To run a successful pub/restaurant, you need to have a constant supply of fresh and high-quality ingredients. However, purchasing inventory can be expensive, particularly for smaller establishments or at times when there are food shortages. A business loan can help cover these costs, allowing you to focus on providing excellent food and service to your customers.

- Marketing and Advertising: In today’s competitive market, it’s vital to invest in marketing and advertising to promote your pub/restaurant and attract new customers. A business loan can help fund these efforts, allowing you to expand your reach and grow your customer base.

No matter your needs, there is a funding option to help you achieve your goals.

How do unsecured loans work?

An unsecured business loan works in the same way as a regular business loan where repayments are made monthly, weekly or daily depending on your agreement. Loan terms can be anywhere between one month to six years according to your business needs.

The loan can be used for almost any expense in the best interest of the business. Businesses usually use these loans for growth and development, refurbishment, capital expenditure or stock. Some business owners and borrowers also use unsecured loans to consolidate other types of debt they have if the loan terms are more favourable.

Unlike secured loans, ‘unsecured’ means your loan is not secured against any personal or business assets, such as property, equipment, vehicles or machinery. An unsecured loan will most likely require a personal guarantee from one or multiple directors.

.svg)

Get a free, no obligation quote

Apply in minutes, there’s no impact on your credit score and you’ll get a free, no obligation personalised quote in hours. Regulated by the FCA: 831395

How much would you like to borrow?

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Prefer to talk? Call us on 01371870815

.svg)

How the process works

[1]

Enquire and check eligibility

Enquire in under 30 seconds to find out if your business is eligible for funding. We only need basic information about your business.

Check eligibility now

[2]

Get matched to lenders

Our LendTech technology will compare over 50 lenders and match you with the most suitable finance options.

Check eligibility now

[3]

Obtain funding in 48 hours

Once you have fully submitted your proposal, one of our funding specialists will discuss the available options and help get you funded.

Check eligibility now

Get a quote, fast

Lending period

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Growth Guarantee Scheme

An unsecured business loan backed by the government. Ideal for businesses looking to grow and expand.

- Amount£25,001 to £750,000

- TermsUp to 6 year terms

- InterestFrom 10% per annum

Start growing

Unsecured Business Loans

A flexible, unsecured business loan with no security on assets or property. Ideal for growth, cashflow or working capital needs.

- Amount£10,000 to £750,000

- TermsUp to 6 year terms

- InterestFrom 6.9% per annum

Get unsecured loan

Asset Finance

Whether you are looking to purchase machinery, equipment or vehicles, this could be the ideal solution for your business.

- Amount£5,000 to £750,000

- TermsUp to 6 years

- InterestFrom 6% per annum

Finance assets

Revolving Credit Facilities

Looking to have a facility where you can drawdown funds when and if you require them, this could be the perfect facility for you.

- Amount£1,000 to £1,000,000

- TermsUp to 3 years

- InterestFrom 1.5% per month

Access credit line

VAT/Tax Loans

Have an upcoming Vat or Tax bill? This could be the perfect facility to keep cashflow healthy and never have to make a big chunky HMRC payment again.

- Amount£10,000 to £750,000

- TermsUp to 1 year term

- InterestFrom 1% per month

Get VAT loan

Merchant Cash Advances

A perfect solution for businesses that take over £10k per month in card/online sales. Rather than paying a fixed monthly payment, repayments are taken as a % of future card sales.

- Amount£10,000 to £750,000

- TermsVariable

- InterestNo APR

Get cash advance

Secured Business Loans

Are you a new start-up business or are you looking to invest a larger sum into your business? By using a property as security, we can lend larger amounts over longer terms.

- Amount£25,000 to £2,000,000

- TermsUp to 15 years

- InterestFrom 10% per annum

Get secured loan

Small Business Loans

Compare small business loans to assist with purchasing stock, upgrading equipment, or just general working capital requirements.

- Amount£10,000 to £750,000

- TermsUp to 6 years

- InterestFrom 6.9% per annum

Get small business loan

.svg)

Guides to help you make the best financial decisions

Compare business funding options today, quickly and easily

Browse our range of business funding options to find out more and discover the one that best suits your business.

Compare funding options

Prefer to chat? Call us on 01371870815 to speak to our experts.

.svg)