Our LendTech platform lets you:

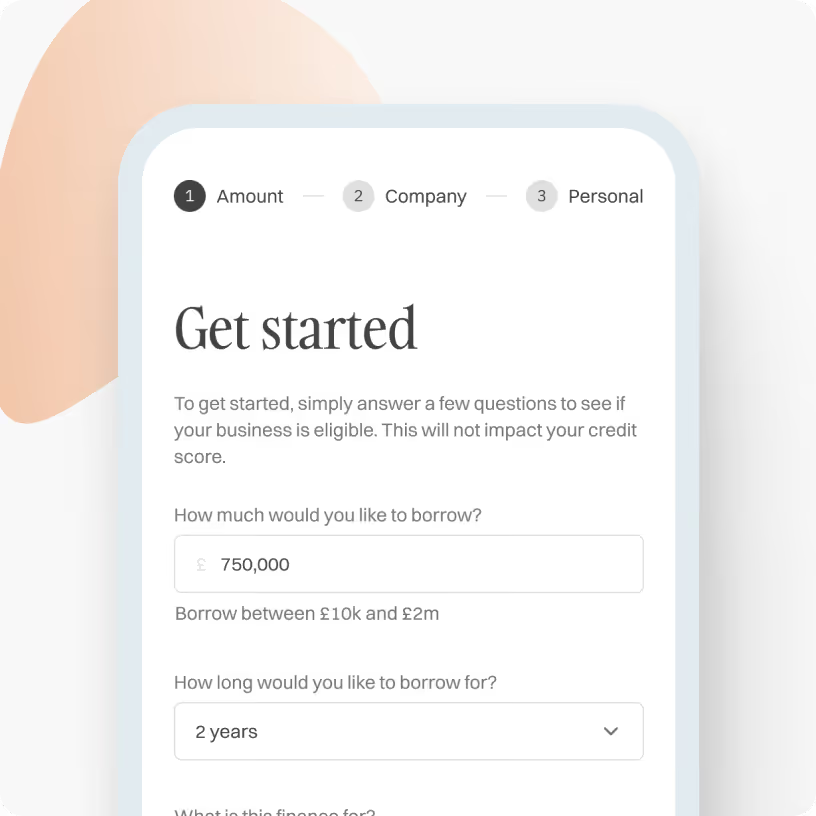

Check eligibility in 30 seconds

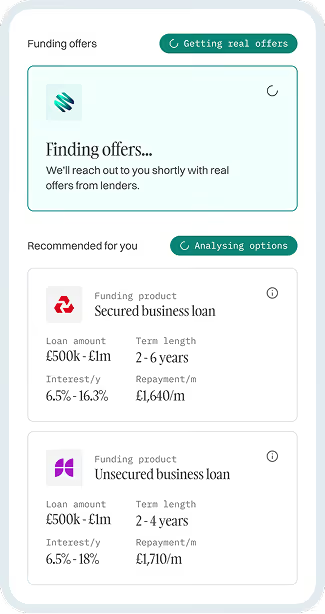

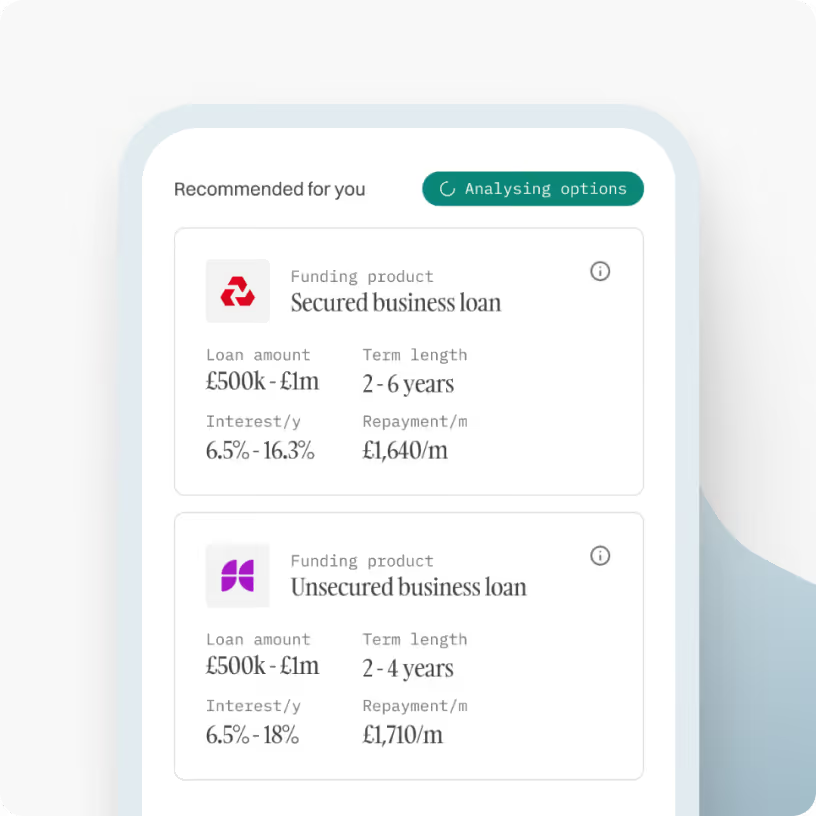

Match with 50+ lenders

Get indicative offers in 5 mins

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

About revolving credit facility

A revolving credit facility will allow your UK business to access an agreed limit of funds whenever necessary. At Aurora Capital, we can pair your business with a trusted provider of revolving credit so that you can benefit from accelerated business growth.

.svg)

What is a revolving credit facility?

A revolving credit facility is a line of credit that allows a UK business to access and repay funds as and when needed. It works in a similar way to an overdraft or credit card.

It’s a short-term alternative funding option that remains accessible once you’ve repaid what you’ve borrowed, so you don’t need to reapply for new credit if you need it.

This facility can act as a financial safety net because it remains available whenever your business needs funds. There is no need to wait for several days or weeks, as you would with other types of business loans, so in the event of an emergency, you can access the funds you need immediately.

Revolving facility credit can help if your business has minor cash flow issues. It allows you to continue operating without disrupting your day-to-day operations.

Key features

- Suitability: Any business looking for flexible funding that they can draw down multiple times a year.

- Purpose: Revolving credit is unrestricted and can be used for any business expense.

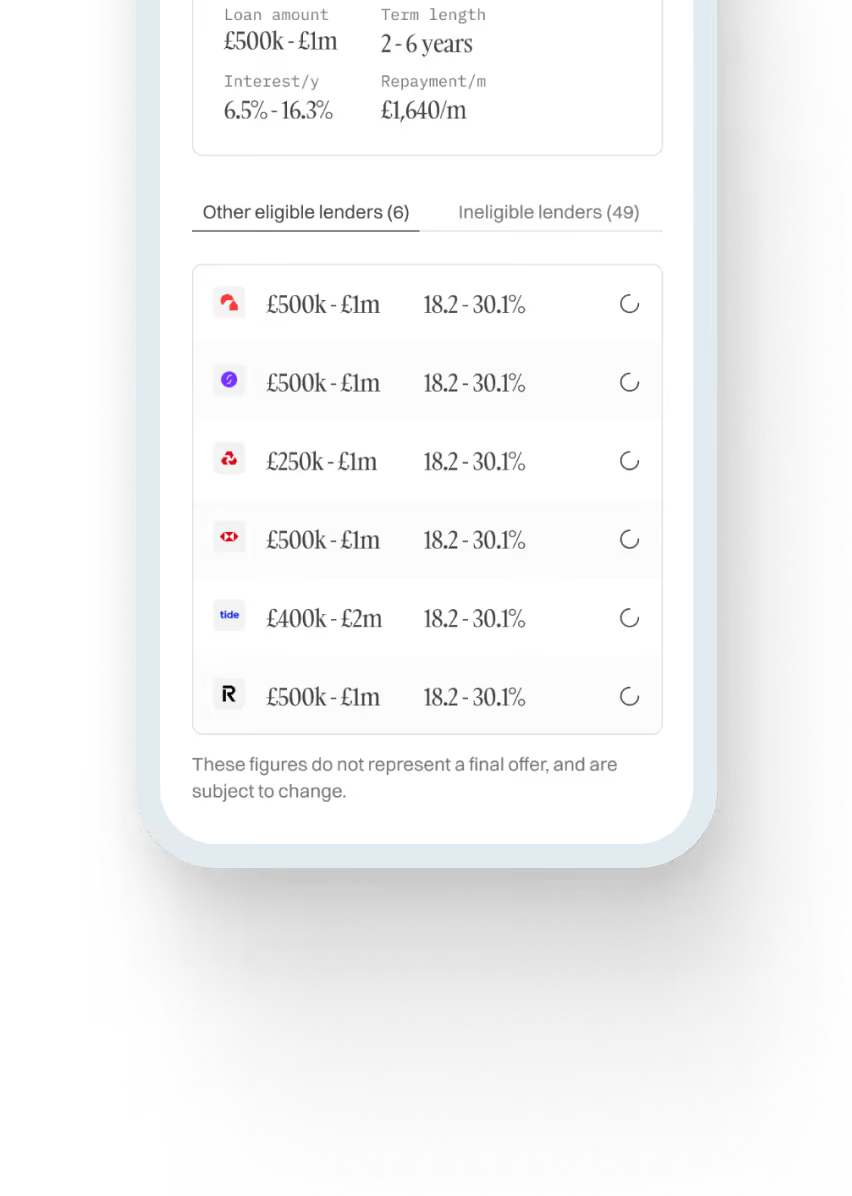

- Amount: Loans range from £10k to £2m. The exact amount you can borrow will vary based on your affordability and the lender.

- Term: Up to 2 years. This will depend on the length of time the business has been trading and its creditworthiness.

- Cost: Lenders charge a daily or monthly interest rate on the money you use. Alternatively, some charge a single fixed fee per drawdown.

- Security: Personal guarantees may be required, but this will depend on the business’s creditworthiness.

- Speed: Applications can be processed within 24 hours of receiving a full proposal, and we can pay out within 48 hours.

How does revolving credit work?

Here’s an overview of how getting a revolving line of credit for your business could work:

- You apply for a revolving credit facility and agree on a credit limit with the lender. This will be based on your needs, but the limit may be restricted depending on your creditworthiness.

- The lender will set a fixed interest rate that you’ll be charged on any amount you withdraw from the credit line. Interest rates typically start from 7%, but some lenders set a fixed fee per withdrawal instead of interest.

- Once agreed, you can request to withdraw from your credit facility within 48 hours.

- The repayment terms will vary depending on the lender. You may need to make repayments weekly or monthly, and some will allow you to pay off the interest only.

- Revolving credit facilities are available for up to two years, but you may be able to extend your agreement if necessary.

Since you only pay interest on what you borrow, your payments will probably be irregular, unlike when you borrow a lump sum of money and are charged interest immediately.

Most terms for revolving credit facilities last up to two years, and provided you have paid on time throughout, you’ll often be eligible for renewal.

Revolving credit facilities are similar to a business overdraft since you can access the revolving line of credit repeatedly as long as you continue to pay off your balance.

Get a free, no obligation quote

Apply in minutes, there’s no impact on your credit score and you’ll get a free, no obligation personalised quote in hours. Regulated by the FCA: 831395

How much would you like to borrow?

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Prefer to talk? Call us on 01371870815

.svg)

Frequently asked questions

What is revolving credit used for?

A revolving credit facility is completely unrestricted and can be used for any business expense. Whether you need to buy stock, hire more staff, or pay bills, a revolving credit business loan could be the perfect choice for your business.

Is my business eligible for a revolving credit facility?

The specific lending criteria will vary from lender to lender. However, there are some standard eligibility requirements you will need to meet to qualify. Most lenders will check:

- Your business is registered and based in the UK

- Your cash flow

- Your business credit score

- Your trading history

Lenders will examine these factors to assess your risk to them. The main thing they will want to understand is how much cash is regularly flowing into your business bank account.

This means that if you’re after a small facility, a lender might look only at your bank account—an advantage if you’re a new company, but you’ll need to have been trading for more than three months.

Revolving credit facilities are generally short-term arrangements, so if you’ve struggled to find credit, you might have more success with this type of product.

Pros and cons of revolving credit

Revolving credit facilities can be a useful funding option for your business, but it’s important to understand the pros and cons before you apply.

Pros of revolving credit

- Flexibility: You can use the facility when needed and don’t have fixed repayments like with a term business loan.

- Pay only for what you need: You only pay interest on the money you use, not the total amount of credit.

- Quick access: You can usually be accepted within 24 hours of applying, and funds can be in your account within 48 hours.

- No early repayment charges: You can repay what you’ve borrowed whenever you want, so there are no charges for clearing the balance early to reduce the interest you pay.

- No security required: You won’t need to secure the credit you borrow against any business assets as part of your application.

Cons of revolving credit

- Higher cost: Although they can be cheaper than credit cards, the interest rates on revolving credit facilities tend to be higher than most fixed-term business loans.

- Short-term: Revolving credit facilities aren't suitable for long-term funding because they are only available for a short period and are designed to cover short-term shortfalls.

- Fees and penalties: You may need to pay additional fees to set up the facility, and there may be penalties for things like missing payments.

- Personal guarantee: The lender may ask for a personal guarantee when you apply, which means you will be liable for any debt if your business defaults on the credit.

- Credit score impact: Revolving credit loans can seriously impact your credit score if your repayments are not well managed.

Why use a revolving credit facility?

A revolving loan facility gives your business access to flexible funding that can help manage cash flow and take advantage of opportunities without taking out multiple loans. This type of credit is beneficial for:

- Managing cash flow: If your income is seasonal or your customers pay on long terms, a revolving credit facility can help cover any gaps and keep your operations running.

- Covering unexpected expenses: Quick access to funds means you can address urgent repairs, resolve supplier issues, or manage sudden increases in demand without disrupting your plans.

- Taking advantage of opportunities: Having a source of credit you can access at short notice lets you move quickly, whether it’s a time-limited deal on stock, a new project, or a growth initiative.

- Avoiding multiple loan applications: Instead of applying for new finance each time you need extra funding, a revolving credit facility is an ongoing credit line you can use repeatedly.

Because it’s designed to be drawn and repaid as needed, a revolving credit facility can be a cost-effective way to maintain business flexibility and reduce strain on your finances.

Can you get revolving credit with bad credit?

Many lenders are willing to offer a revolving credit facility even if your business credit history isn’t perfect. These facilities are often more flexible than traditional loans, making them a viable option for businesses that have struggled to secure financing elsewhere.

If your credit score is low, the lender will typically review your recent financial activity, including bank statements and cash flow, to assess whether the facility is affordable.

In some cases, a personal guarantee may be required. This means you agree to take personal responsibility for repayment if the business is unable to pay. Still, it can help you secure approval and access better rates or a higher limit.

Can I repay a revolving credit facility early?

Yes, you can repay at any time without paying a penalty. The lender will outline Your repayment terms when your application is approved.

How long can I borrow with revolving credit facilities?

You can borrow for a maximum of 2 years. The length of time will depend on your time trading and your credit information, which will be assessed following your application.

If you have managed the facility well, you may be able to extend your agreement at the end of the term, but this will be at the lender's discretion.

How much can I borrow with revolving credit facilities?

You can borrow up to £2 million with a revolving credit facility and use these funds at any time. The size of your credit limit will be calculated following your initial application.

What is the difference between a revolving credit facility and a business loan?

The main difference between revolving credit and a term business loan is that you can withdraw the funds as and when you need them and, therefore, only pay interest on what you need.

You also don’t have a fixed repayment schedule and can repay what you’ve borrowed at any time. For these reasons, revolving credit facilities are a more flexible funding solution than a fixed-term loan.

A business loan is usually a better option for long-term borrowing, as the interest rate is usually lower. You can potentially borrow larger amounts and spread the cost over many years.

What is a revolving credit facility used for?

Unlike a traditional business loan or agreement, you can use revolving credit funds for any business expense.

Revolving credit is a useful option if your business’s cash flow is irregular or sporadic, as it can help you cover any gaps. Unlike a generic business loan, you’re only charged for what you use, which makes it a great backup option for unexpected expenses.

Revolving credit for business usually comes with interest costs; however, they tend to be lower than credit card or overdraft rates. The exact interest rates you are offered for your revolving facility credit will depend on the lender.

How does repayment work for revolving credit facilities?

Repayment terms can vary from lender to lender. Some only require you to pay the interest for the duration of the contract, whereas others require the interest and capital to be repaid from the drawn funds.

You will usually need to make repayments every month, but this may differ depending on the term length of your facility.

How much does a revolving credit facility cost?

The cost of your revolving credit will depend on the interest rate charged, the fees payable, and how much you borrow from the facility. Interest rates can start from 7%, but the lender will decide your rate based on factors like your creditworthiness, the credit limit you want, and the term of the facility.

Some providers take a single fixed fee from the drawdown amount without ongoing interest. Others charge ongoing interest on the used funds on either a daily or weekly basis.

Are revolving credit facilities secured?

You do not need to secure revolving credit against any business assets. This means you won’t risk losing an asset if you cannot keep up with your repayments.

However, some lenders may request a personal guarantee when applying for revolving credit. This means you would be personally liable for any debts if your business cannot repay the facility's outstanding balance.

Don’t see your question? Send us a message or call us on 01371870815 to speak to one of our funding specialists quickly.

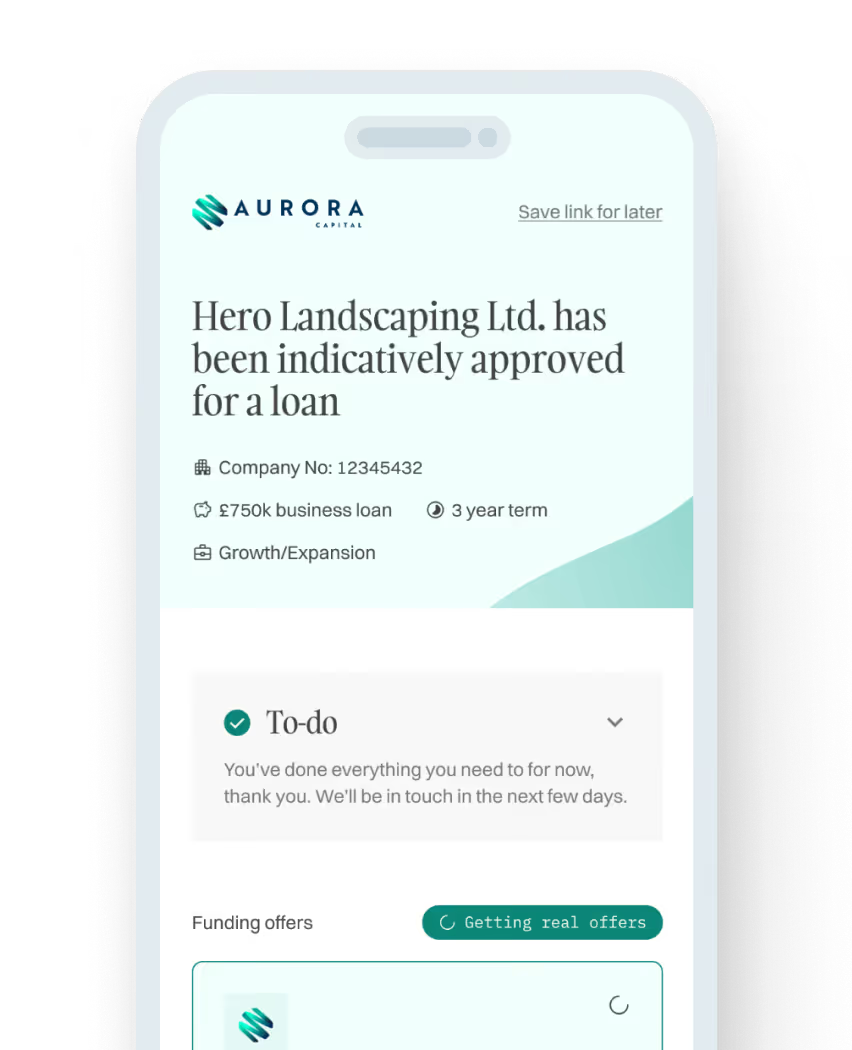

How the process works

[1]

Enquire and check eligibility

Enquire in under 30 seconds to find out if your business is eligible for funding. We only need basic information about your business.

Check eligibility now

[2]

Get matched to lenders

Our LendTech technology will compare over 50 lenders and match you with the most suitable finance options.

Check eligibility now

[3]

Obtain funding in 48 hours

Once you have fully submitted your proposal, one of our funding specialists will discuss the available options and help get you funded.

Check eligibility now

No items found.

No items found.

No items found.

Get a quote, fast

Lending period

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Growth Guarantee Scheme

An unsecured business loan backed by the government. Ideal for businesses looking to grow and expand.

- Amount£25,001 to £750,000

- TermsUp to 6 year terms

- InterestFrom 10% per annum

Start growing

Unsecured Business Loans

A flexible, unsecured business loan with no security on assets or property. Ideal for growth, cashflow or working capital needs.

- Amount£10,000 to £750,000

- TermsUp to 6 year terms

- InterestFrom 6.9% per annum

Get unsecured loan

Asset Finance

Whether you are looking to purchase machinery, equipment or vehicles, this could be the ideal solution for your business.

- Amount£5,000 to £750,000

- TermsUp to 6 years

- InterestFrom 6% per annum

Finance assets

Revolving Credit Facilities

Looking to have a facility where you can drawdown funds when and if you require them, this could be the perfect facility for you.

- Amount£1,000 to £1,000,000

- TermsUp to 3 years

- InterestFrom 1.5% per month

Access credit line

VAT/Tax Loans

Have an upcoming Vat or Tax bill? This could be the perfect facility to keep cashflow healthy and never have to make a big chunky HMRC payment again.

- Amount£10,000 to £750,000

- TermsUp to 1 year term

- InterestFrom 1% per month

Get VAT loan

Merchant Cash Advances

A perfect solution for businesses that take over £10k per month in card/online sales. Rather than paying a fixed monthly payment, repayments are taken as a % of future card sales.

- Amount£10,000 to £750,000

- TermsVariable

- InterestNo APR

Get cash advance

Secured Business Loans

Are you a new start-up business or are you looking to invest a larger sum into your business? By using a property as security, we can lend larger amounts over longer terms.

- Amount£25,000 to £2,000,000

- TermsUp to 15 years

- InterestFrom 10% per annum

Get secured loan

Small Business Loans

Compare small business loans to assist with purchasing stock, upgrading equipment, or just general working capital requirements.

- Amount£10,000 to £750,000

- TermsUp to 6 years

- InterestFrom 6.9% per annum

Get small business loan

.svg)

Guides to help you make the best financial decisions

Compare business funding options today, quickly and easily

Browse our range of business funding options to find out more and discover the one that best suits your business.

Compare funding options

Prefer to chat? Call us on 01371870815 to speak to our experts.

.svg)