All business needs options

Invoice Finance

Unlock cash tied up in unpaid invoices with flexible facilities designed to improve cash flow and help access working capital faster.

Our LendTech platform lets you:

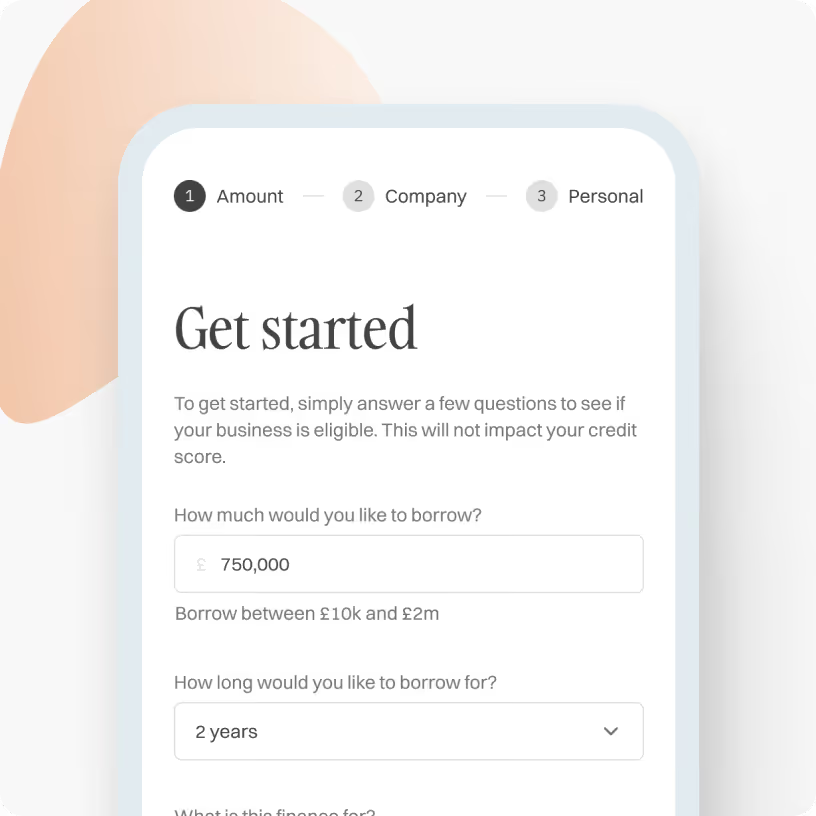

Check eligibility in 30 seconds

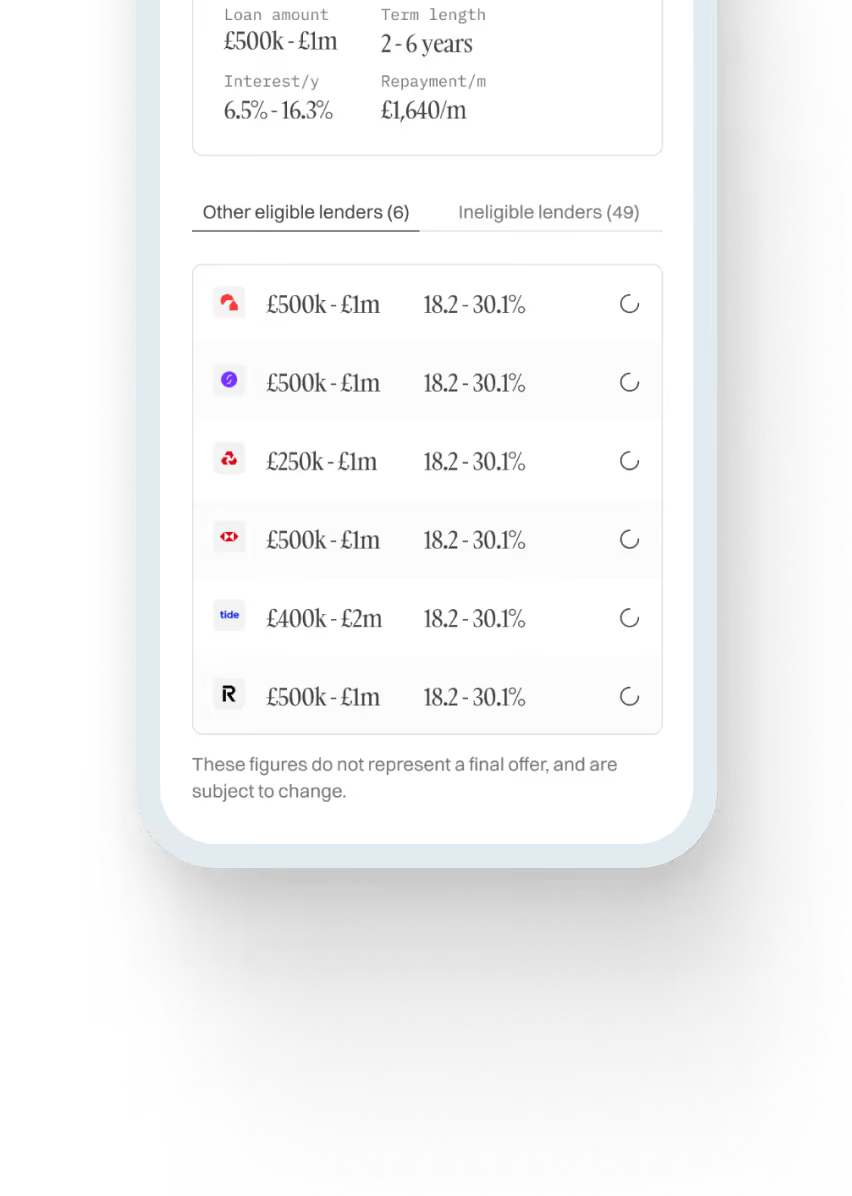

Match with 50+ lenders

Get indicative offers in 5 mins

Check eligibility

Applying won't affect your credit score

Apply in minutes

Free, no-obligation quote

No effect on credit score

Get a quote, fast

Lending period

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Business invoice finance

Invoice finance can provide your business with a cash flow injection by releasing capital tied up in unpaid invoices. Discover the different invoice financing options and prepare to grow your business by having quicker access to the funds you’re owed.

What is invoice finance?

It’s a type of business loan that allows your company to release money from unpaid invoices. An invoice finance provider advances you a percentage of the cash value of invoices you’re waiting to be paid by your customers.

It can take up to 90 days to complete an invoice, which can impact your business’s cash flow. Invoice finance can give you quick access to the money you’re owed, sometimes within 48 hours, so your business operations aren’t impacted.

The invoice finance providers we work with can pay up to 90% of the value of your invoices the minute they are raised. Once the invoice payment has been settled, you will receive the balance minus interest and fees.

Key features

- Suitability: Businesses that have payment terms beyond 30 days and who are selling to other businesses (B2B).

- Purpose: Used to strengthen ongoing cash flow.

- Amount: Up to 90% of invoices can be advanced on day one. This will depend on the number of invoices you have and how long your business has been trading.

- Term: Invoice financing is a rolling facility with no fixed term.

- Cost: Between 1% and 4% of the invoice value. Some products charge an annual or subscription fee.

- Security: Some invoice funding solutions will be unsecured, but they may ask for a personal guarantee.

- Speed: Applications can be processed and funding arranged within 48 hours.

.svg)

Get a free, no obligation quote

Apply in minutes, there’s no impact on your credit score and you’ll get a free, no obligation personalised quote in hours. Regulated by the FCA: 831395

How much would you like to borrow?

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Prefer to talk? Call us on 01371870815

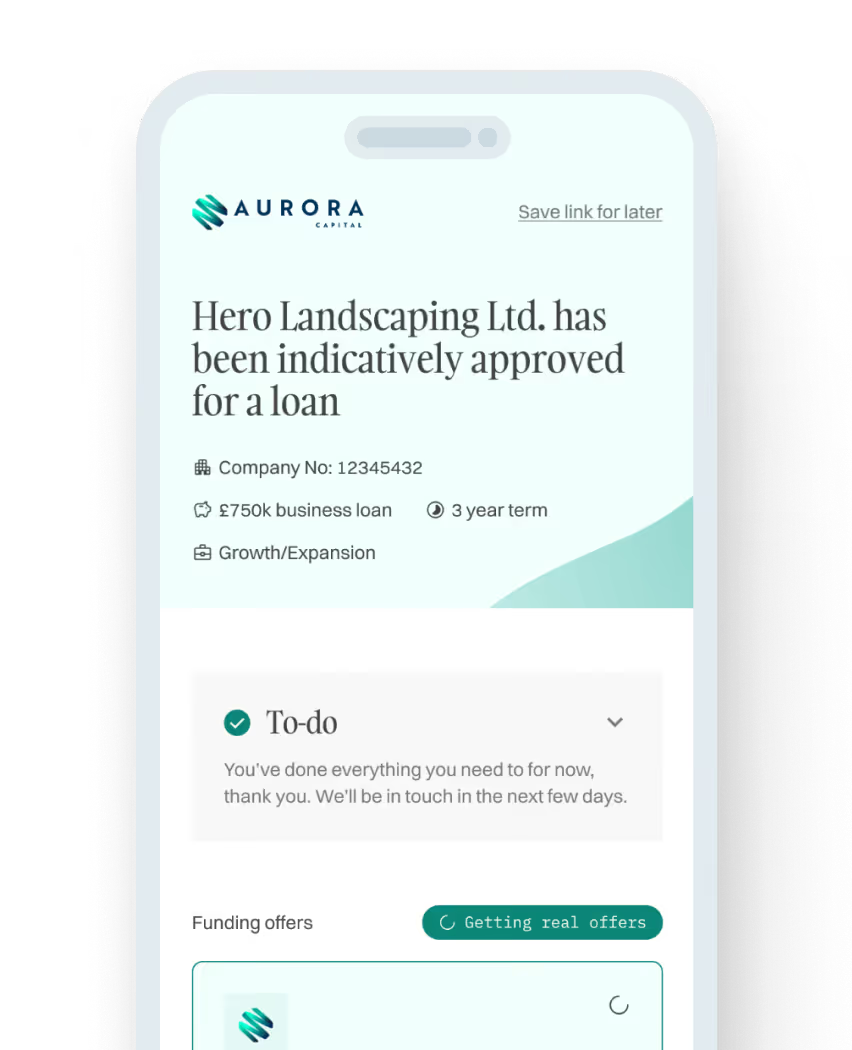

How the process works

[1]

Enquire and check eligibility

Enquire in under 30 seconds to find out if your business is eligible for funding. We only need basic information about your business.

Check eligibility now

[2]

Get matched to lenders

Our LendTech technology will compare over 50 lenders and match you with the most suitable finance options.

Check eligibility now

[3]

Obtain funding in 48 hours

Once you have fully submitted your proposal, one of our funding specialists will discuss the available options and help get you funded.

Check eligibility now

No items found.

No items found.

No items found.

How much could you borrow?

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Apply in minutes

Free, no-obligation quote

No effect on credit score

Growth Guarantee Scheme

An unsecured business loan backed by the government. Ideal for businesses looking to grow and expand.

- Amount£25,001 to £750,000

- TermsUp to 6 year terms

- InterestFrom 10% per annum

Start growing

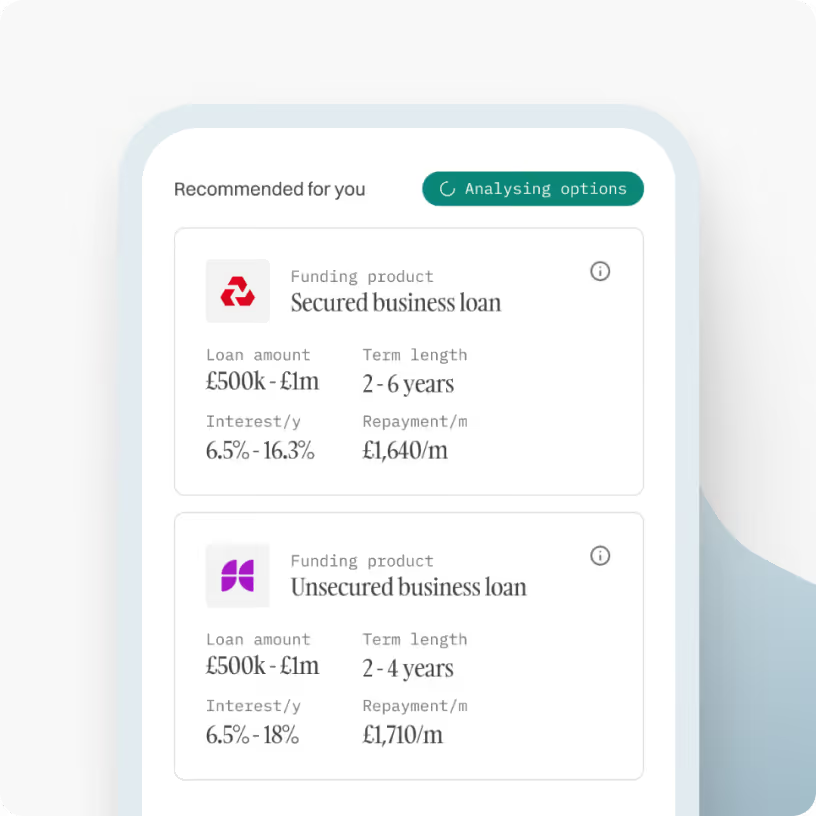

Unsecured Business Loans

A flexible, unsecured business loan with no security on assets or property. Ideal for growth, cashflow or working capital needs.

- Amount£10,000 to £750,000

- TermsUp to 6 year terms

- InterestFrom 6.9% per annum

Get unsecured loan

Asset Finance

Whether you are looking to purchase machinery, equipment or vehicles, this could be the ideal solution for your business.

- Amount£5,000 to £750,000

- TermsUp to 6 years

- InterestFrom 6% per annum

Finance assets

Revolving Credit Facilities

Looking to have a facility where you can drawdown funds when and if you require them, this could be the perfect facility for you.

- Amount£1,000 to £1,000,000

- TermsUp to 3 years

- InterestFrom 1.5% per month

Access credit line

VAT/Tax Loans

Have an upcoming Vat or Tax bill? This could be the perfect facility to keep cashflow healthy and never have to make a big chunky HMRC payment again.

- Amount£10,000 to £750,000

- TermsUp to 1 year term

- InterestFrom 1% per month

Get VAT loan

Merchant Cash Advances

A perfect solution for businesses that take over £10k per month in card/online sales. Rather than paying a fixed monthly payment, repayments are taken as a % of future card sales.

- Amount£10,000 to £750,000

- TermsVariable

- InterestNo APR

Get cash advance

Secured Business Loans

Are you a new start-up business or are you looking to invest a larger sum into your business? By using a property as security, we can lend larger amounts over longer terms.

- Amount£25,000 to £2,000,000

- TermsUp to 15 years

- InterestFrom 10% per annum

Get secured loan

Small Business Loans

Compare small business loans to assist with purchasing stock, upgrading equipment, or just general working capital requirements.

- Amount£10,000 to £750,000

- TermsUp to 6 years

- InterestFrom 6.9% per annum

Get small business loan

.svg)

Guides to help you make the best financial decisions

Compare business funding options today, quickly and easily

Browse our range of business funding options to find out more and discover the one that best suits your business.

Compare funding options

Prefer to chat? Call us on 01371870815 to speak to our experts.

.svg)