Peer-to-Peer Business Loans

By

Aurora Capital

March 31, 2026

.svg)

.svg)

What is peer-to-peer lending?

Peer-to-peer lending, also known as P2P lending, is an innovative form of loan that eliminates banks and their fees.

It acts like an online marketplace that connects businesses looking for finance with individuals and groups of investors who want to lend their money for a return.

Instead of borrowing from a bank, businesses receive funding directly from one or more private investors through a regulated platform.

For borrowers, this can mean faster decisions, more flexible terms, and better value compared to traditional business loans. It’s an attractive alternative to savings accounts for investors, offering the potential for significantly higher returns.

Key features

- Suitability: Businesses looking for an alternative to high-street lending, often with a faster online process and potentially more flexible criteria.

- Purpose: Any legitimate business purpose, including working capital, stock, equipment, refurbishment, marketing, and growth.

- Amount: Typically £10,000 to £500,000, depending on the platform, your affordability, and credit profile.

- Term: Usually short to medium-term (often 6 months up to around 5–6 years), depending on the platform and product.

- Cost: Interest rates and fees vary by platform and risk. Some platforms may also charge arrangement or admin fees.

- Security: Many P2P business loans are unsecured, but a personal guarantee may be required. Some platforms also offer secured P2P lending.

How does peer-to-peer lending work?

Peer-to-peer lending allows businesses to borrow money directly from individual investors through an online platform. Here’s a breakdown of how the process typically works:

- Work out your borrowing needs: Start by understanding how much funding your business needs, what it will be used for, and how long you’ll need to repay it.

- Choose a P2P platform: Research FCA-regulated peer-to-peer platforms specialising in business lending. Compare interest rates, fees, eligibility criteria and customer reviews before deciding where to apply.

- Complete an application: Fill out a short online application form. You’ll typically need to provide details about your business, financial information, and the loan amount and term you’re looking for.

- Review your loan offers: Once approved, your loan request is listed and matched with investors. You may receive multiple offers; compare terms, interest rates, and repayment schedules carefully.

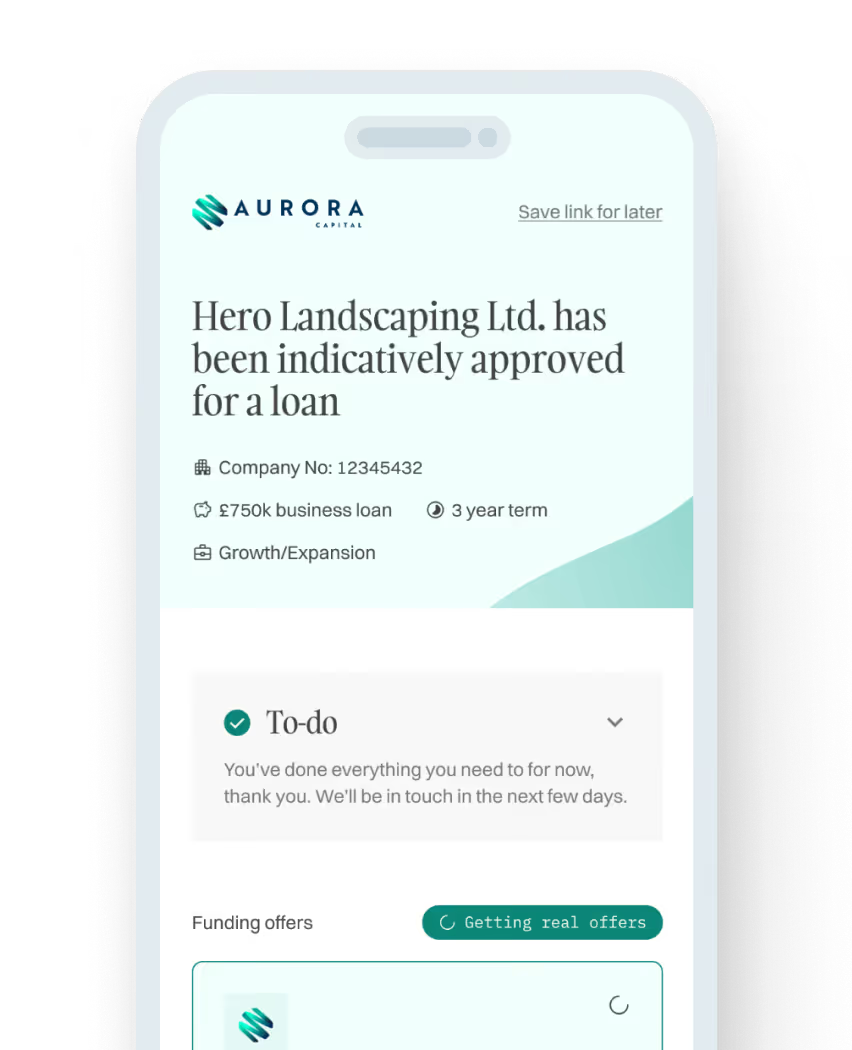

- Accept an offer and get the funds: Choose the best offer for your business. After accepting, funds are transferred to your bank account, usually within 1 to 3 working days.

- Repay the loan: Repay the loan in monthly instalments over the agreed term. The platform handles repayments and sends them on to the investors backing your loan.

Peer-to-peer lending for businesses is designed to mean that borrowers and lenders can access better rates than they would get through a traditional lender or savings account.

Get a free, no obligation quote

Apply in minutes, there’s no impact on your credit score and you’ll get a free, no obligation personalised quote in hours. Regulated by the FCA: 831395

How much would you like to borrow?

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Prefer to talk? Call us on 01371870815

How the process works

[1]

Enquire and check eligibility

Enquire in under 30 seconds to find out if your business is eligible for funding. We only need basic information about your business.

Check eligibility now

[2]

Get matched to lenders

Our LendTech technology will compare over 50 lenders and match you with the most suitable finance options.

Check eligibility now

[3]

Obtain funding in 48 hours

Once you have fully submitted your proposal, one of our funding specialists will discuss the available options and help get you funded.

Check eligibility now

Frequently asked questions

Pros and cons of peer-to-peer business loans

There are several benefits to using P2P lending over traditional business finance, but there are also risks you need to be aware of. Here are the pros and cons of peer-to-peer loans you need to consider before you apply:

Pros of P2P business loans

- Competitive interest rates

- Easier access to funding

- Diverse investment opportunities

- Fast decisions

- Flexible loan amounts available

Cons of P2P business loans

- Arrangement fees could apply

- A personal guarantee may be required

- Platform and regulatory risk

- Loan amounts may be limited

Read our guide for an in-depth look at the pros and cons of peer-to-peer business loans.

How can you use a peer-to-peer loan?

Peer-to-peer business loans are very flexible, and once approved, you can use the funds for almost any legitimate business purpose. Here are some of the most common ways businesses use peer-to-peer finance:

- Working capital: It can cover day-to-day operational expenses like payroll, rent, utilities, or supplier payments. This can be especially useful during seasonal drops in revenue or short-term cash flow gaps.

- Purchasing stock or equipment: You can use a P2P loan to buy new inventory, materials, or machinery to help fulfil larger orders, increase production, or improve operational efficiency.

- Expansion or refurbishment: Open a new location, upgrade your existing premises, or invest in improvements that support long-term growth and customer experience.

- Marketing campaigns: Fund advertising, digital marketing, or lead generation strategies to reach new customers and grow your revenue.

- Investing in staff or training: Hire new employees, upskill your team, or bring in consultants to help develop new initiatives or business development.

You may be asked to outline how you plan to use the funds during the application process, but you don’t need to have a detailed plan for every penny.

What matters is that the loan is used to support your business goals, and you can comfortably manage the repayments

Is a peer-to-peer loan right for your business?

Peer-to-peer business loans can be a flexible and accessible way to raise finance, especially if you want a faster and potentially more affordable alternative to going through a bank.

This type of lending can be beneficial if your business has a good trading history, consistent revenue, and a clear plan for how the funds will support your growth.

Peer-to-peer borrowing can also be appealing if you’ve struggled to access finance through mainstream lenders or you want more flexibility around how the loan is structured.

However, peer-to-peer loans may not be suitable for every business. If you’re looking to borrow a large sum, need a long repayment period, or you’d feel more comfortable borrowing from an established lender, P2P may not be the right option.

If your business has a poor credit record or unpredictable cash flow, it might also be harder to get approved, or you may be offered higher interest rates.

As with any type of business finance, it’s important to consider how the repayments will affect your cash flow and whether the loan supports your business objectives

Peer-to-peer lending alternatives

If peer-to-peer lending isn’t the right fit for your business, you can consider a range of alternative finance options. Each one works differently and is suited for different business needs and requirements.

Unsecured business loans

Unsecured business loans let you borrow without putting up any assets as collateral. This makes them a popular choice for businesses with good cash flow but no valuable assets.

They can be used for almost any purpose, from bridging cash flow gaps to funding marketing campaigns or hiring staff. Approval is typically based on your trading history, revenue, and business credit score.

Secured business loans

Secured loans allow you to borrow larger amounts using business assets like a UK property as security. Because lenders have collateral as a safety net, interest rates are often lower than those for unsecured lending.

This type of loan is well-suited to established businesses looking to fund major investments or consolidate existing debts on improved terms.

Asset finance

Asset finance helps you spread the cost of purchasing business assets, like machinery, vehicles, or new technology. Instead of paying upfront, you make regular repayments while using the asset to generate income.

It’s an effective way to manage cash flow while still accessing the tools you need to grow. Some businesses also use asset refinance to unlock capital tied up in existing equipment or vehicles.

Merchant cash advance

A merchant cash advance gives you a lump sum based on your business’s card sales, with repayments taken automatically as a percentage of daily or weekly takings.

This means you repay more when business is busy and less when it’s quiet, providing a flexible alternative to fixed monthly payments. It’s especially useful for retail, hospitality, or e-commerce businesses with high card transactions.

Revolving credit facility

A revolving credit facility works like a flexible credit line you can draw from as and when needed. You’re only charged interest on the funds you use, making it an ideal option for managing cash flow or covering unexpected expenses.

Unlike a traditional term loan, a revolving credit facility allows funds to become available again once repaid, providing ongoing access to capital when your business needs it.

Is peer-to-peer lending regulated in the UK?

P2P lending platforms are regulated by the Financial Conduct Authority (FCA) in the UK.

How quickly can I get a peer-to-peer business loan?

It depends on the platform and your application, but P2P lending can be quicker than traditional options. Some decisions can be near-instant, and funds may be available within a couple of days.

How much can I borrow with a peer-to-peer business loan?

Loan sizes vary by platform and by your business finances. As a general guide, P2P loans can range from hundreds up to £500,000, with higher amounts sometimes available for the right case.

What can I use peer-to-peer business finance for?

Most platforms allow flexible use for legitimate business needs, such as working capital, stock, equipment, hiring, marketing, and expansion or refurbishment.

Do I need security for a P2P business loan?

Not always. Many P2P business loans are unsecured, but you may still be asked for a personal guarantee. Some platforms also offer secured options, typically linked to property or other assets.

What fees do peer-to-peer platforms charge?

Some charge arrangement or administration fees, and there may be late payment charges depending on the agreement. Always check the full costs before accepting an offer.

Can a start-up get a peer-to-peer business loan?

Sometimes, but businesses with a financial track record often access better rates and terms. If you’re a new business, you may be offered smaller amounts or higher rates, and you’ll usually need a strong plan and clear affordability.

Don’t see your question? Send us a message or call us on 01371870815 to speak to one of our funding specialists quickly.

Compare business funding options today, quickly and easily

Browse our range of business funding options to find out more and discover the one that best suits your business.

Compare funding options

Prefer to chat? Call us on 01371870815 to speak to our experts.

.svg)