Is a Small Business Loan Secured or Unsecured?

By

Aurora Capital

April 7, 2026

.svg)

.svg)

Small business loans can be either secured or unsecured. A secured loan is backed by an asset, such as property, while an unsecured loan does not require security.

The right option for your business depends on how much you need to borrow, how quickly you need the funds, and what your business can afford to repay.

If you apply for an unsecured loan, you usually won’t need to have a property for security, but you may still be asked for a personal guarantee.

If you apply for a secured loan, you will need to have a property to use as security, most commonly a UK residential or commercial property.

What is a secured small business loan?

A secured business loan is a type of business finance that’s backed by a UK property. You borrow a lump sum and repay it over an agreed term, usually in monthly instalments.

Having security to fall back on reduces the lender’s risk, which means secured loans can offer lower interest rates and longer terms than unsecured borrowing, depending on your application and the value of the security.

Secured business loans are often used for larger or longer-term investments, such as expansion, refurbishments, acquisitions, or refinancing. However, it’s important to understand that the property is at risk if you can’t repay the loan.

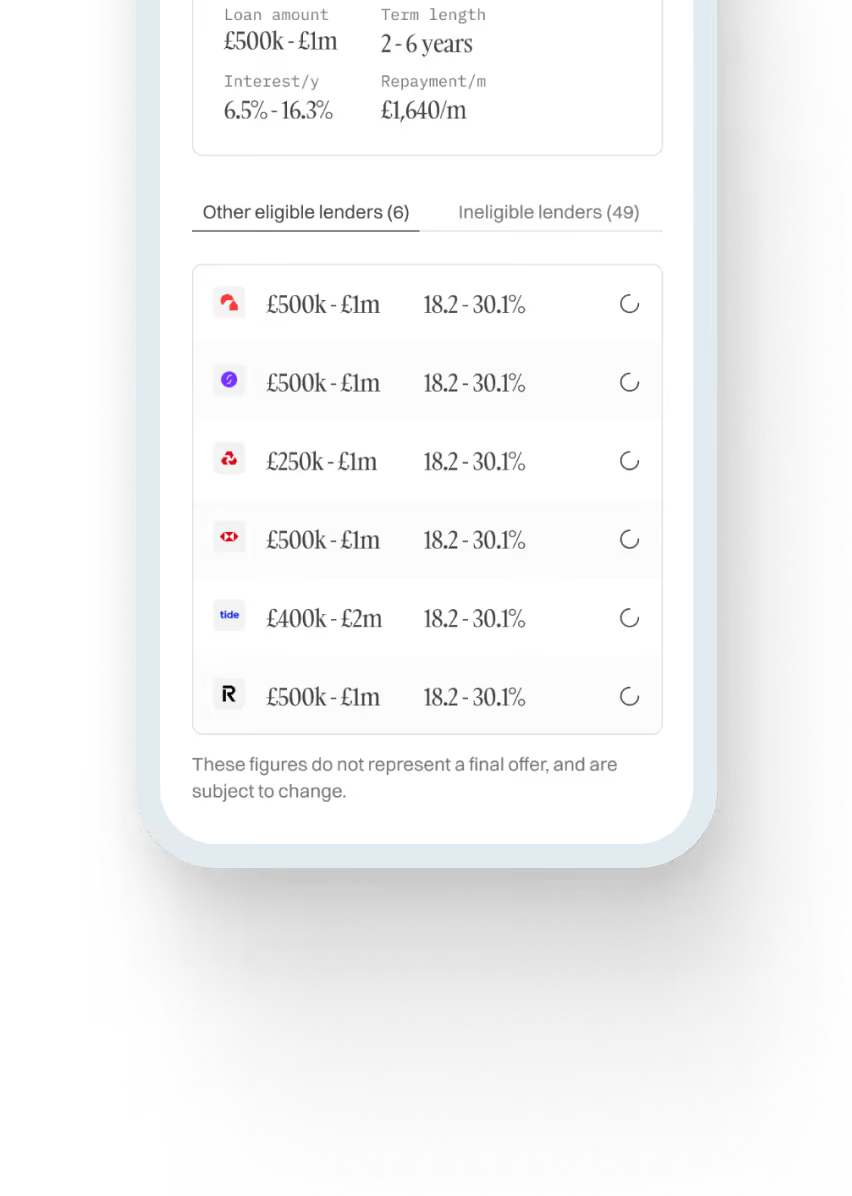

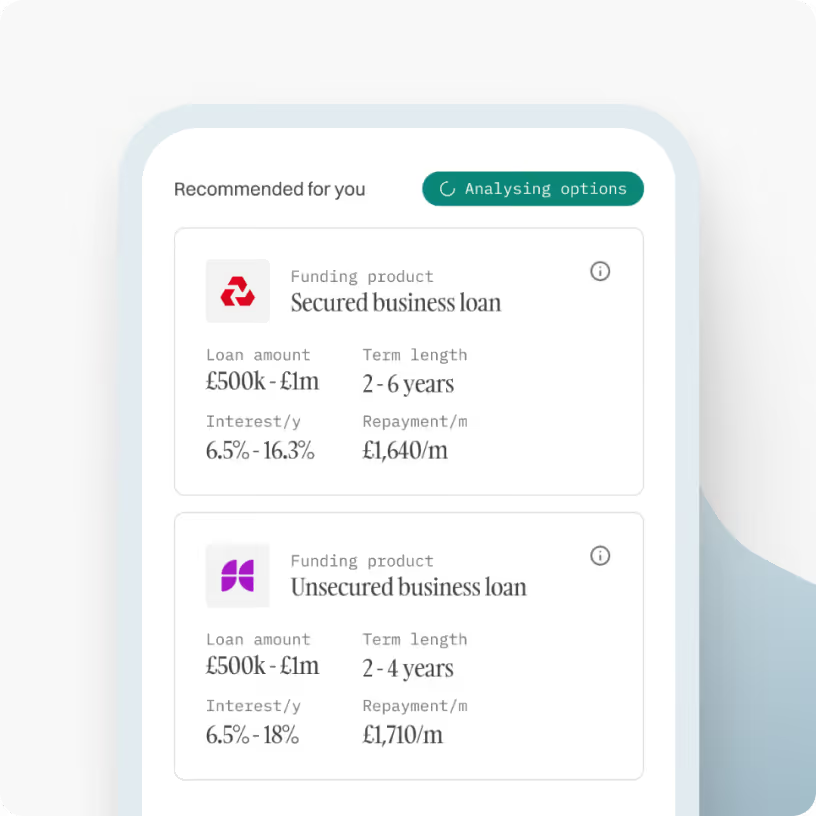

- Loan amount: £25,000 to £2 million

- Loan term: 2 to 15 years

- Cost: Interest rates start from 10% per annum (valuation or legal fees may apply)

- Loan to value: Up to 75% LTV (depending on the lender)

- Security: Secured against a UK residential or commercial property

- Speed: Usually slower than unsecured loans because valuations and legal checks are often required

What is an unsecured small business loan?

An unsecured business loan doesn’t require an asset, such as property, as collateral. This means your business or personal assets won’t be at risk if you’re unable to keep up with the loan repayments.

Because the lender doesn’t have security, unsecured loans can be quicker to arrange than secured borrowing, but interest rates can be higher depending on your credit score, affordability, and trading performance.

Unsecured business loans can be used for a range of business needs, including working capital, stock purchases, marketing spend, hiring, or covering short-term business costs.

- Loan amount: £10,000 to £500,000

- Loan term: 1 month to 6 years

- Cost: Interest rates start from 8.9% per annum

- Security: No asset security required

- Speed: Often faster than secured borrowing, with funds potentially available in days

Differences between secured and unsecured business loans

Secured and unsecured small business loans both give you access to funding, but they work in different ways. Understanding the differences can help you understand which type of small business loan might be best for you.

Security and guarantees

A secured business loan is backed by an asset, most commonly UK property. If you can’t keep up with repayments, the lender has a legal claim over the security.

An unsecured business loan does not require collateral. However, you may need to provide a personal guarantee, which means you will be personally liable if the business cannot repay the loan.

Borrowing amounts and terms

Secured loans are often used for larger borrowing and longer terms, because the security reduces the lender’s risk. This can make them suitable for bigger investments such as expansion, acquisitions, refurbishments, or refinancing.

Unsecured loans are usually used for smaller amounts over shorter terms. They can work well for working capital, stock, marketing spend, or time-sensitive costs.

Interest rate and other costs

Because secured loans are lower risk for the lender, interest rates can be lower than unsecured borrowing, depending on the strength of your application and the value of the property you’re using as security.

Unsecured loans can be more expensive. Rates and fees vary, so it is always worth comparing the total cost of borrowing, not just the headline interest rate.

Speed and application requirements

Unsecured loans are typically quicker to arrange because there is no asset to value and no legal work linked to security. Applications can often be assessed within 24 hours, and funds can be sent within 48 hours.

Secured loans can take longer, often several days or weeks, as valuing the asset and completing legal checks can add steps to the process.

Pros and cons of secured small business loans

Pros of secured small business loans

- Interest rates can be lower than unsecured borrowing

- Suitable for larger loan amounts, often with longer terms

- Monthly repayments can be lower when spread over a longer period

- Can be used for most business purposes

Cons of secured small business loans

- Requires an asset as security, usually a UK property

- The asset is at risk if repayments aren’t maintained

- Can take longer to arrange due to valuations and legal checks

- May involve additional costs such as valuation or legal fees

Pros and cons of unsecured small business loans

Pros of unsecured small business loans

- No property or asset security required

- Often quicker to arrange than secured borrowing

- Fixed monthly repayments make budgeting easier

- Can be used for a wide range of business costs

Cons of unsecured small business loans

- Interest rates can be higher than secured borrowing

- Loan amounts and terms are often lower and shorter than secured loans

- A personal guarantee may be required

- Missed repayments can impact your credit profile and ability to borrow in the future

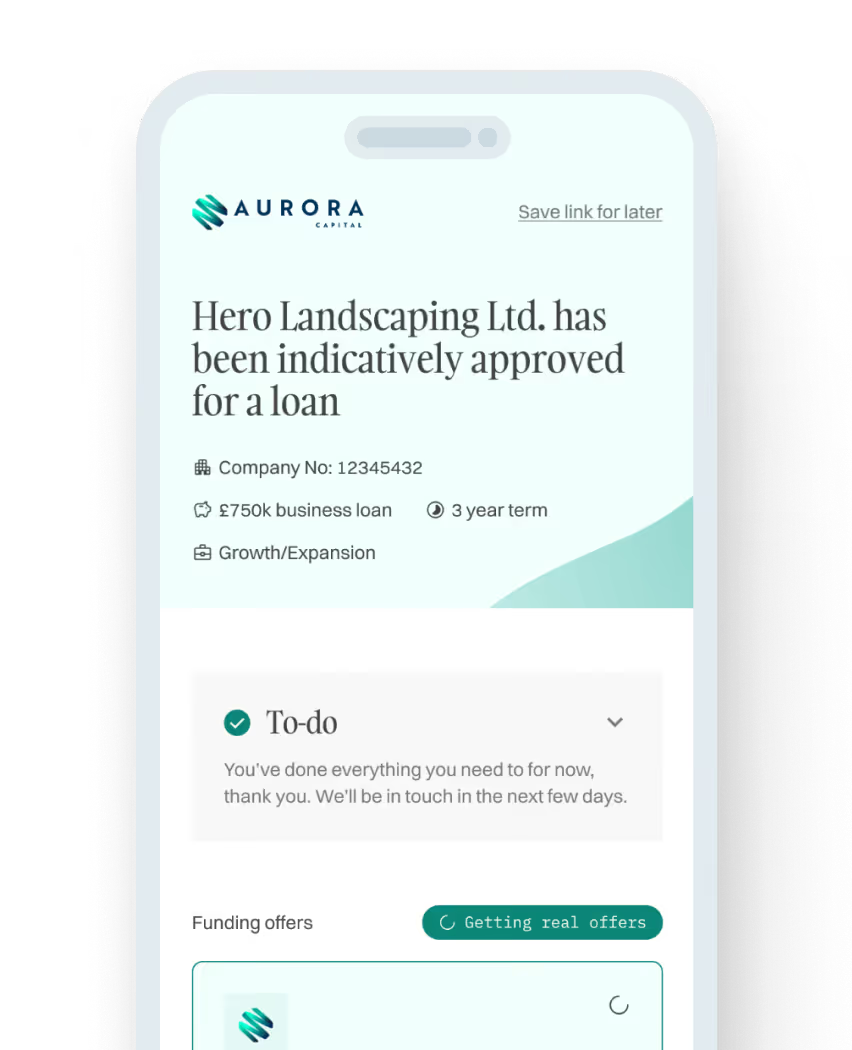

Get a free, no obligation quote

Apply in minutes, there’s no impact on your credit score and you’ll get a free, no obligation personalised quote in hours. Regulated by the FCA: 831395

How much would you like to borrow?

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Prefer to talk? Call us on 01371870815

How the process works

[1]

Enquire and check eligibility

Enquire in under 30 seconds to find out if your business is eligible for funding. We only need basic information about your business.

Check eligibility now

[2]

Get matched to lenders

Our LendTech technology will compare over 50 lenders and match you with the most suitable finance options.

Check eligibility now

[3]

Obtain funding in 48 hours

Once you have fully submitted your proposal, one of our funding specialists will discuss the available options and help get you funded.

Check eligibility now

Frequently asked questions

Common mistakes to avoid when choosing a loan

Here are some common mistakes small businesses make when deciding between a secured and an unsecured loan:

- Borrowing based on the maximum available rather than what you can afford to repay

- Choosing a longer term to reduce monthly repayments, without considering the total cost

- Using short-term borrowing for long-term projects can add pressure to cash flow

- Not factoring in quieter months, seasonal trading, or delays in customer payments

- Borrowing too little and needing another loan soon after, which can increase costs

How to choose between a secured and unsecured loan

If you run a small business, the right choice comes down to the purpose of the loan, how much you need to borrow, timing, and your attitude to risk.

If you need a small or mid-sized loan for a short-term need, such as cash flow, stock, payroll, or a time-sensitive bill, an unsecured loan may be the simplest and quickest option because it doesn’t require property security.

If you need to borrow more for a large-scale project such as expansion, refurbishment, or an acquisition, a secured loan may be a better fit. It can support higher amounts and longer terms, and rates can be lower.

Whichever option you choose, focus on affordability first and aim for a loan with repayments that your business can comfortably afford. If you’re considering a secured loan, make sure you’re comfortable with using a property as collateral.

How to apply for a secured or unsecured loan

Applying for a small business loan is usually straightforward. In most cases, you’ll be asked for the same information whether you choose a secured or unsecured option.

For both secured and unsecured loans, you’ll usually need to provide:

- Full name of the business

- Personal details of the business director and any guarantors

- Permission to perform personal searches

- The amount you want to borrow

- The term of the borrowing

- The reason the funds are required

- The last 6 months’ bank statements

- Company accounts (if available)

If you’re applying for a secured business loan, you will also need to provide details of the UK property being used as collateral. Valuations and legal checks may be required, which can delay the process.

At Aurora Capital, we help small businesses compare secured and unsecured loans and match them with a suitable lender. You can apply online in minutes and receive a free, no-obligation quote.

If you’re not sure which route is right, contact our team today, and they can talk you through your options and help you choose funding that fits your needs and what you can afford to repay.

Don’t see your question? Send us a message or call us on 01371870815 to speak to one of our funding specialists quickly.

Compare business funding options today, quickly and easily

Browse our range of business funding options to find out more and discover the one that best suits your business.

Compare funding options

Prefer to chat? Call us on 01371870815 to speak to our experts.

.svg)