What are trade loans and how can they work for my business?

By

Aurora Capital

June 4, 2026

.svg)

.svg)

It’s a scenario that many small businesses in the UK will be familiar with. You need stock, supplies or materials to keep trading, but your cash flow is tied up in day-to-day costs, slow-paying customers, or long payment terms. This is exactly where trade finance can help.

Whether you have purchase orders stacking up, seasonal demand to meet, or an opportunity to buy stock at a discount, trade loans are designed to keep you trading confidently without putting further pressure on your working capital.

Keep reading to discover more about what trade loans are, how they work and when they’re worth considering for your business.

What is a trade loan?

Also known as a trade finance loan, a trade loan is a type of business funding used to support everyday trade activity. Most commonly, the purchase of stock or raw materials, paying suppliers and bridging the gap between outgoing payments and incoming revenue are all potential scenarios where a trade loan can help.

How do trade loans work?

Trade loans can cover a few different funding structures. Some businesses use a flexible credit facility as a line of credit that they draw down when they need to pay suppliers. Others use asset-backed options where the amount available is linked to stock, invoices or other business assets.

1. Flexible access to funds when you need them

This option is similar to a revolving credit facility, where your business can draw funds, repay and borrow again within an agreed limit. As an ongoing facility you can dip in and out as your business needs evolve, while only paying interest on the amount you actually withdraw. This is perfect for managing cash flow and short-term expenses without having to apply for a new loan each time you need access to funding.

In a trade context, this can be used to:

- Pay suppliers on time (even if customers pay later)

- Buy inventory ahead of demand

- Smooth seasonal cash flow swings

- Move quickly on time-limited stock deals

2. Funding linked to business assets

Trade loans can also be structured around asset-based lending (ABL). ABL is a type of business loan where the amount you can borrow is linked to the value of eligible assets your business owns. This kind of funding is often secured against invoices, inventory or equipment.

That matters for trade because:

- Stock and inventory can be eligible assets

- The available funding can scale as trading and asset values grow

- It can be used to cover gaps between paying suppliers and receiving payment

ABL facilities may require ongoing reporting on asset values. Lenders typically monitor asset values, and you can be asked to report monthly or even more frequently. The available limit may be reduced if reporting is late or asset values change.

Where does export finance fit?

If your business imports goods or sells overseas, trade finance can also extend into export finance with specialist funding structures designed to support cross-border trading. While the mechanics vary - and often depend on country risk, currency risk and documentation - the goal is still to help you fulfil orders and manage the timing gap between shipping goods and receiving payment.

What can trade loans be used for?

Trade loans are most useful when cash flow timing is the problem, not profitability.

Purchasing stock or inventory

If you need to buy ahead of demand due to seasonal peaks, promotions or new product launches, trade finance can help you secure inventory without tying up all your working capital.

Paying suppliers on time

Supplier relationships matter. Trade finance loans can help you meet supplier terms even when your own customers are on 30, 60 or 90-day payment cycles.

Managing cash flow gaps

A line of credit and asset-based lending can both support day-to-day working capital and cover gaps between outgoing payments and incoming revenue.

Funding larger orders

Asset-based lending can be used to buy stock or fund larger orders, particularly when the facility is linked to business assets and designed to support day-to-day operations.

Supporting growth without disrupting working capital

Trade finance for businesses is often used to fund growth moments that put strain on your cash flow. Expanding product lines, increasing order volume or entering new markets are all common business cases for asset-based lending.

Things to remember

If your challenge is timing rather than demand, trade finance for businesses can be a practical way to keep operations moving and protect working capital. And if you’re planning to expand internationally, trade finance can also support cross-border sales and purchasing through export finance structures, helping you manage the added complexity of overseas trading.

Get a free, no obligation quote

Apply in minutes, there’s no impact on your credit score and you’ll get a free, no obligation personalised quote in hours. Regulated by the FCA: 831395

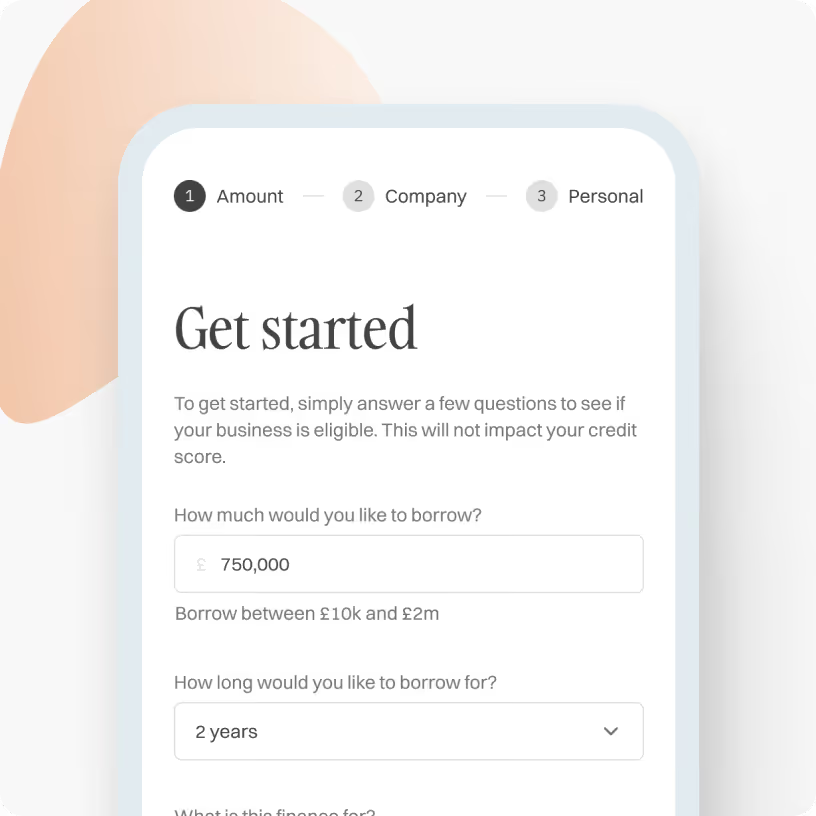

How much would you like to borrow?

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Prefer to talk? Call us on 01371870815

How the process works

[1]

Enquire and check eligibility

Enquire in under 30 seconds to find out if your business is eligible for funding. We only need basic information about your business.

Check eligibility now

[2]

Get matched to lenders

Our LendTech technology will compare over 50 lenders and match you with the most suitable finance options.

Check eligibility now

[3]

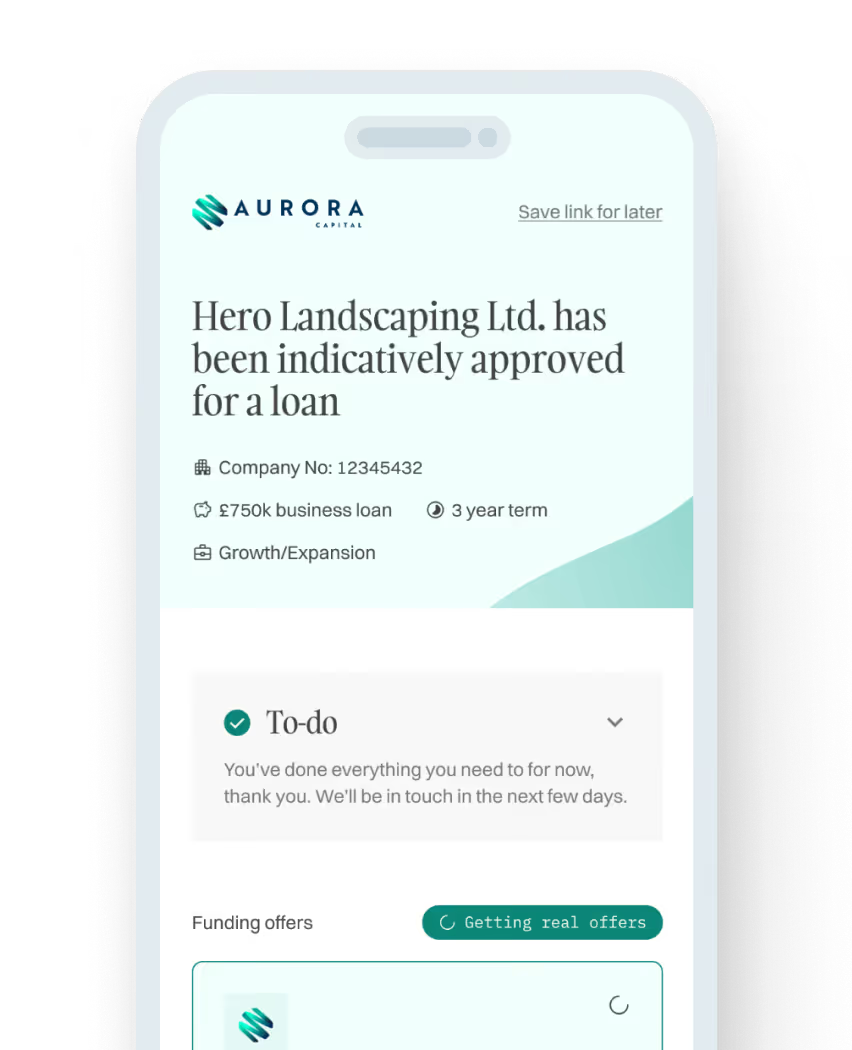

Obtain funding in 48 hours

Once you have fully submitted your proposal, one of our funding specialists will discuss the available options and help get you funded.

Check eligibility now

Frequently asked questions

What are the different types of trade loans?

Revolving credit facilities

Draw funds. Repay. Redraw. Similar to an overdraft-style structure, revolving credit facilities are set up as an agreed credit line with ongoing access to funds, typically over a term ranging from three months to a couple of years. it’s ideal when supplier payments and inventory purchasing happen regularly but unpredictably.

Business line of credit

A business line of credit (LOC) is a type of revolving credit facility that offers flexible access to funds up to an agreed limit. You only pay interest only on what you borrow. It can be used to cover short-term costs and manage cash flow without tying up working capital.

Asset-based lending

Asset-based lending enables your business to borrow funds linked to the value of the business assets you have in-hand. It can be structured as a revolving facility or a term loan to support cash flow and stock purchasing, especially when your business holds valuable inventory or has receivables.

Export finance and cross-border trade support

If you import goods or export products, export finance can help manage cross-border cash flow timing. For example, paying suppliers abroad while waiting for overseas buyers to pay. Even if you’re not trading internationally today, it’s useful to know that trade finance can grow with your business if you expand into new markets.

How do I qualify for a trade loan?

Qualification depends on the lender and the trade finance structure. But the foundation is usually consistent: lenders want to see that the business is trading steadily and can manage repayments. Typical criteria lenders may look for, include:

- 6–12 months of trading history

- Regular monthly turnover (often from £5,000 upwards)

- A separate business bank account

- A reasonable business credit score

- Supporting financial documents such as bank statements or tax returns

For asset-based lending, eligibility is closely tied to the assets you hold. They will need to be valued and verified with the results submitted alongside your trading history.

What you can do to improve your chances

If you want to move quickly and increase your approval odds, it helps to:

- Keep clean, up-to-date bank statements and management accounts

- Maintain strong records for stock, invoices, and debtor balances (especially for asset-backed options)

- Be clear on what you need funding for (stock purchase, supplier payment, working capital)

- Match the product to your need (flexible facility vs fixed loan)

Is a trade loan right for my business?

Trade finance can be a smart solution, but it’s not one-size-fits-all. The right fit depends on your cash flow pattern and how your business buys and sells.

A trade loan may be right if:

- You regularly buy stock or materials and need flexibility

- Your customers pay on terms, creating a gap between outgoing and incoming cash

- You want to take advantage of time-sensitive stock opportunities

- Your business is growing, and you need working capital that can scale

You may want to consider alternatives if:

- You need a large, one-off investment (for example, new premises or major equipment) rather than funding stock cycles

- You don’t have a predictable repayment capacity over the short term

- You don’t have the asset base or reporting capability needed for asset-based structures

Don’t see your question? Send us a message or call us on 01371870815 to speak to one of our funding specialists quickly.

Compare business funding options today, quickly and easily

Browse our range of business funding options to find out more and discover the one that best suits your business.

Compare funding options

Prefer to chat? Call us on 01371870815 to speak to our experts.

.svg)